If you have high liquidity sitting in banks, the Sukuk bond is a risk-free, tax-exempt investment worth considering.

It’s a Sharia-compliant bond that works differently from regular (conventional) bonds.

What makes Sukuk special is its strong appeal to institutional investors, which makes it harder for everyday Nigerians to buy directly, except in the secondary market.

This high demand also shows that Sukuk is a more stable and trusted investment option.

This article uncovers everything you need to know about Sukuk bonds, including a step-by-step guide on investing.

How Sukuk Bonds Work in Nigeria

According to Oluwagbenga Magbagbeola, CEO at Sycamore Investment and Asset Management Ltd, a guest on BusinessFront TV’s Equity Market program,

“The Sukuk bond is gaining massive traction because it fills a gap in Nigeria’s market—ethical, asset-backed investing, and it’s not just for Muslims. With as little as ₦10,000, anyone can invest in infrastructure-backed instruments that avoid interest and offer stable, long-term returns. The recent ₦300 billion issuance recorded over ₦2.2 trillion in subscriptions.”

Sukuk bonds are investment instruments that comply with Islamic finance principles, meaning they avoid interest (riba), gambling (maysir), and uncertainty (gharar).

Unlike conventional debt-based bonds offering fixed interest payments, Sukuk are backed by tangible assets and generate returns through profit-sharing or rental income.

Here’s how the investment generally works:

Let’s assume the Federal Government wants to build a major express road connecting Lagos to Abuja, but doesn’t want to borrow money the usual way (where it has to pay interest).

Instead, it used a Sukuk bond, which follows Islamic rules and avoided interest.

Assuming the government needs N100 billion to complete this road project, it doesn’t just ask the public to lend it money.

Instead, it creates something called a Sukuk certificate and says:

“If you buy this Sukuk, you will become part-owner of this road project. And for the next 7 years, we will pay you a share of the income or rent we get from using the road (at coupon rate). After 7 years, we’ll buy back your share and return your full money (bullet repayment).”

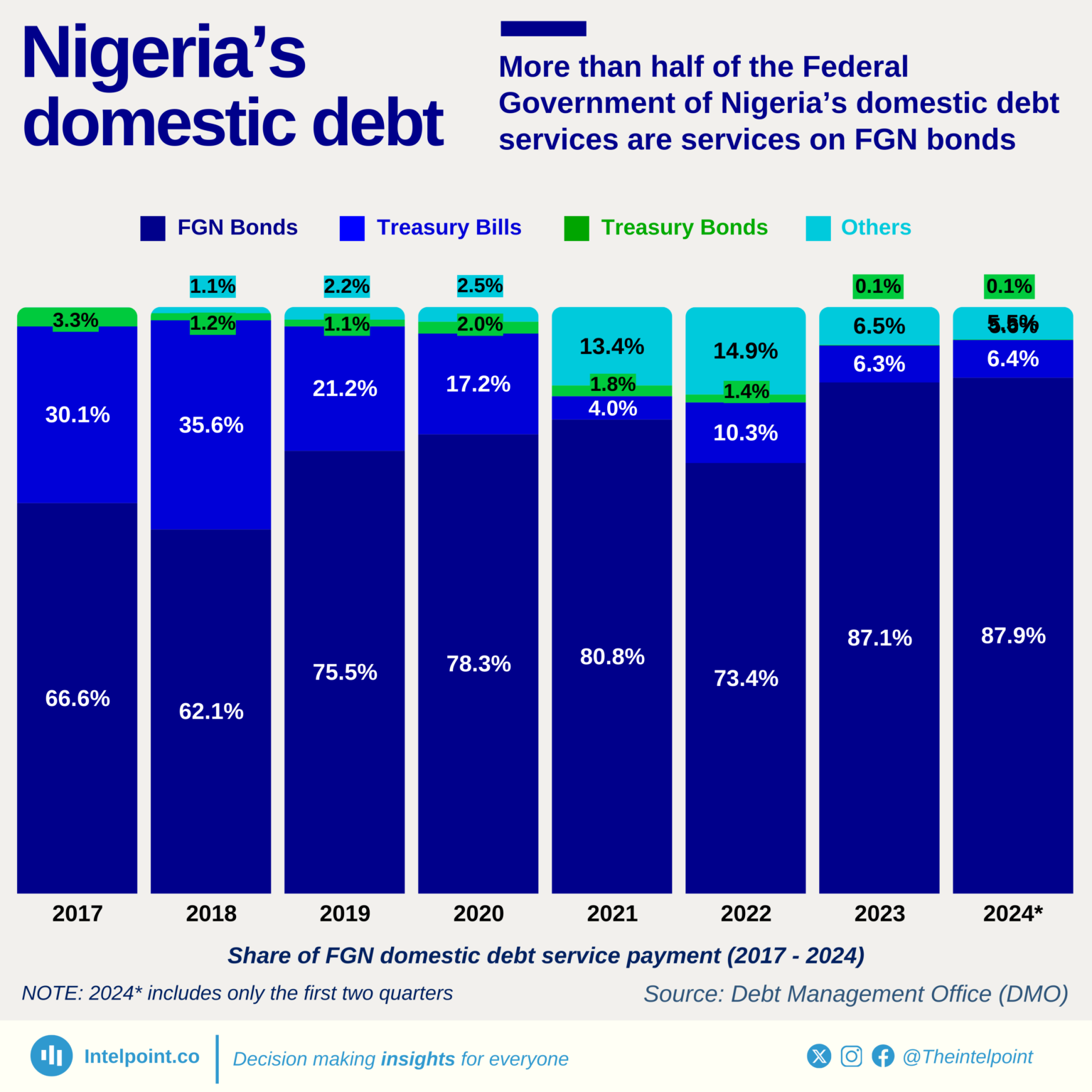

FGN Bonds dominate Nigeria’s domestic debt service payments, rising from 66.6% in 2017 to 87.9% in 2024. This reflects a growing reliance on long-term debt financing.

Find more on Intelpoint

- When the Federal Government or another issuer needs funds for a project, instead of borrowing money traditionally, they create a Sukuk issuance backed by a tangible asset (think: road, facilities, or energy project).

- Investors who buy Sukuk certificates are not lending money; they buy an ownership share in the asset or the benefit it generates.

- Over the Sukuk’s term, the asset produces income, such as rent or toll fees, which is distributed to investors as profit, not interest.

- At maturity, the government buys back the asset and returns the principal to the investors.

The annual coupon rate given to investors varies, but the most recent one issued by the FGN was 19.75%, paid every six months.

It also had a minimum investment amount of N10,000.

Role of SPVs, Trustees, and Shariah Advisers

Sukuk can take various structures, each suited to different types of projects.

The most commonly used in Nigeria by the Federal Government (FG) is the Ijara Sukuk, based on a lease contract.

In this model, the issuer sells the asset to investors via a Special Purpose Vehicle (SPV), then leases it back and pays rent regularly, which becomes the investors’ return.

A critical part of the Sukuk structure is the use of an SPV.

This entity was created solely to manage the Sukuk issuance and hold the underlying asset on behalf of the investors. It helps isolate the asset from the issuer’s financial risks.

Alongside the SPV, a trustee is appointed to protect investors’ interests and ensure compliance with the terms of the Sukuk.

A Shariah advisory board is also essential. These Islamic finance scholars vet the Sukuk’s structure, contracts, and purpose to ensure everything aligns with Islamic law.

Other structures of Sukuk include:

- Musharaka: It involves a partnership where profits and losses are shared.

- Mudarabah: This one is a profit-sharing arrangement where one party provides capital and the other expertise

- Istisna: It is often used for construction, where an asset is built, sold, or leased to generate returns.

Regulatory Guidelines: The SEC and Legal Framework

In Nigeria, the Securities and Exchange Commission (SEC) regulates Sukuk under the Investments and Securities Act of 2007, with more specific guidelines outlined in the Sukuk Rules of 2013.

These rules require that every Sukuk be backed by tangible assets and approved by a registered Shariah advisory board.

The issuer must also appoint a trustee and ensure proper risk disclosures are provided to investors.

Apart from the SEC, other institutions play key roles.

The Central Bank of Nigeria (CBN) ensures financial system stability, while the Debt Management Office (DMO) coordinates and issues Federal Government Sukuk.

Meanwhile, international bodies like the Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) and the Islamic Financial Services Board (IFSB) also guide Nigeria’s Sukuk market.

They provide Shariah-compliant accounting and risk management standards.

Benefits and Risks of Sukuk Bonds in Nigeria

Sukuk bonds are backed by tangible assets, making them relatively safer than conventional bonds that depend solely on creditworthiness.

The FG issues most Sukuk in Nigeria through the DMO office, further boosting investor confidence.

However, there are some drawbacks to be aware of. For instance, Sukuks are not as easy to sell quickly (they are less liquid), and big institutional investors snap up most.

Here’s a table that puts the pros and cons of Sukuk bonds in better perspective:

| Pros | Cons |

| Asset-Backed | Not always easy to sell quickly |

| Ethical investing | Longer maturity date (usually 7 years) |

| Tax-favorable | Possible lower returns compared to conventional bonds |

| Government-backed investment option | Institutional buyers dominate public offers |

Who Is Eligible to Invest in FGN Sukuk?

If you’re looking for a safe and ethical way to grow your money, FGN Sukuk offers a stable investment backed by the government.

It’s ideal for people who want returns without dealing with high risks or interest-based products.

Aside from retail investors, the instrument is also open to:

- Households: Individuals and families (local and foreign residents)

- Small businesses: Traders, Merchants, Professional firms, e.t.c

- Associations and Unions: Professional bodies, Cooperative societies, Student Union Governments, Trade Unions, Town Unions, Chambers of Commerce, e.t.c

- Registered religious Bodies: Churches, Mosques, e.t.c

- Educational institutions: Primary, Secondary and Tertiary

- Corporate entities: Banks, Insurance companies, Pension funds, Funds and Asset Managers, e.t.c

- High network individuals

- Government agencies, states and local governments

- High-net-worth individuals, especially those who support socially responsible or faith-aligned investing

- Companies like Noor Takaful Insurance and Salaam Takaful Limited offer Islamic-compliant insurance.

How To Invest in Sukuk Bonds: A Step-by-Step Guide

Sukuk instruments are tradable on platforms such as the Nigerian Stock Exchange (NGX), providing liquidity for investors.

However, if you are particular about Sukuk issued by the Federal Government of Nigeria, stay updated with the DMO office.

They occasionally announce new Sukuk investment opportunities on the website or via the official social media handles.

Step 1: Reach Out to Authorised Sellers

When a new Sukuk offer opens, you can invest by contacting approved channels, such as commercial banks, licensed stockbrokers, or registered investment firms.

These entities help process your subscription.

Sukuk instruments are tradable on platforms like the Nigerian Stock Exchange (NGX).

Like regular bonds, investing directly in a Sukuk bond comes with heavy demands.

It’s no easy feat, from the minimum amount to the required knowledge and time.

A tested alternative is to invest in them through Sukuk funds, mutual funds that pool your cash with others to invest in Sukuk bonds.

Financial platforms like Cowrywise offer such an option.

Step 2: Subscribe During the Offer Period

You can buy into the Sukuk during the subscription window by paying the minimum amount required (usually disclosed in the offer details).

For instance, the recent FGN’s 7-year Al’Ijarah Series VII Sovereign Sukuk had a minimum subscription of N10,000 and a maximum of N100 million for retail investors.

It had an 8-day subscription window before closing.

The Series VII Sovereign Sukuk offered ₦300 billion and recorded an unprecedented subscription level of over ₦2.205 trillion. This represents an excess of 735% subscription.

Step 3: Hold or Sell Later

Once you’ve invested, you can hold your Sukuk until the end of its term and earn rental income over time.

However, if you need quick cash, you can sell your units on the secondary market, though availability might vary.

Step 4: Get Your Money Back at the End

At maturity (typically after 7 or 10 years, depending on sukuk issuance), the government will buy back the Sukuk asset and repay your principal. This is referred to as bullet repayment.

Sukuk Vs Conventional Bonds: Side-by-Side Comparison

Before choosing to subscribe to any Sukuk offering, you should know how they compare to conventional bonds in structure, returns, ownership, risk, etc.

| Feature | Sukuk (Islamic Bonds) | Conventional Bond |

| Structure | Asset-backed; investor owns a share in an asset | Debt-based; the investor lends money to the issuer |

| Compliance | Must follow Islamic (Sharia) law | No religious or ethical compliance required |

| Returns | Profit generated from the asset (e.g., rent, income) | Interest (fixed or variable) paid by the issuer |

| Risk | Generally lower due to asset backing and ethical screening | Depends on the issuer’s credit rating |

| Tradability | Tradable in the secondary market if asset-backed | Freely tradable |

| Popularity | Used by the government for infrastructure funding | Widely used for public and private sector borrowing |

Investing in Sukuk Bond: Tips for Prospective Investors

If you want to get started with FGN Sukuk Bonds, here are important tips to guide you:

1. Check the Sukuk Rating and Safety

Like other investment products, Sukuk bonds are rated for safety and risk.

Agencies like Fitch Ratings, Agusto & Co or GCR provide ratings. A high rating means lower risk.

FGN Sukuk usually has a good rating because the government backs it.

The Director General of the DMO, Ms Patience Oniha, recently emphasised that Nigeria’s recent credit rating upgrade by Fitch Ratings reflects progress in economic and debt management reforms.

2. Understand the Tenure (Maturity Period)

The tenure tells you how long your money will be tied up.

Most FGN Sukuk bonds have a tenure of 7 years, meaning you’ll get your capital back in 7 years.

Only invest money you won’t need urgently.

3. Use Only Authorised Dealers and Issuing Houses

You can’t buy FGN Sukuk just anywhere. Always invest through authorised banks, stockbrokers, or issuing houses listed by the Debt Management Office.

Even after the auctions, investors can access the FGN bonds in the secondary market through any of the broker-dealers on the FMDQ OTC Trading Platform or through Stanbic IBTC Stockbrokers on the Nigerian Stock Exchange (NSE).

The main point is to avoid fraud and record your investment properly.

4. Understand the Returns (Profit)

Instead of interest, you earn rental income on the projects funded by Sukuk based on the coupon rate.

This return is usually fixed and paid every 6 months. For example, if the return is 11%, you’ll get a portion every half-year.

Returns are steady and predictable. That’s why Sukuk is ideal for long-term planning.

Wrapping Up

It’s ironic that despite the ‘investor-appetite’ towards sukuk bonds offered by the “African giant,” Nigeria still battles with record-high inflation and a cost-of-living crisis.

While the economy is yet to fully regain its footing, sub-national and corporate Sukuk issuances are also growing in Nigeria.

Notable examples include the states of Osun and Lagos, Family Homes Ltd, and TAJ Bank Plc, along with private Sukuk issuances by three other subnationals.