As of 2024, stablecoin usage across Africa and the Middle East represented an estimated 6.7% of the total regional GDP, one of the highest adoption rates globally, according to a 2025 International Monetary Fund (IMF) Working Paper. This is a market verdict on the inadequacy of existing infrastructure.

This shows that African users are no longer waiting for a system that fails them, they are simply finding systems that work. When official banking channels are slow and expensive, people find a way around them. By using digital currencies like USDT and USDC, they get instant, guaranteed payments without the risk of money getting stuck in foreign accounts. This volume belongs on African rails, but it will only return when our own systems offer the same speed and value.

The bottleneck to continental prosperity is not a lack of technology, but a failure of the traditional correspondent banking business model. While Africa is home to numerous instant payment systems, most remain digital islands. Unlocking genuine financial inclusion and trade efficiency requires a fundamental transition from a messaging-based correspondent model to a packet-switched Open Payments architecture.

The macroeconomic chokehold

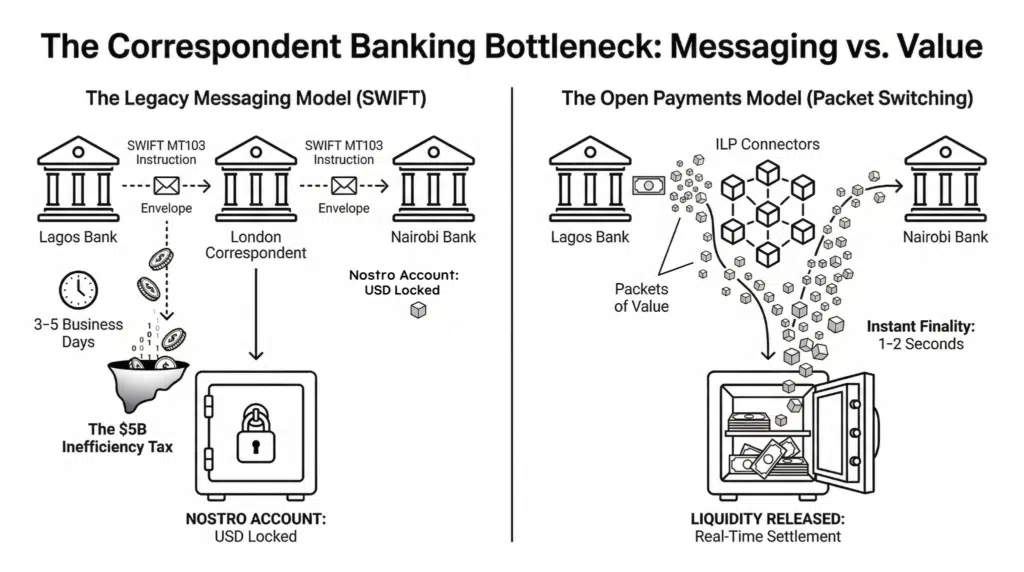

The correspondent banking model, the silent plumbing of international trade, is in a state of terminal decline across Africa. This model relies on Nostro accounts, where a local bank maintains a foreign currency balance at a global correspondent bank to facilitate trades. Between 2020 and 2026, global tier-one banks have rapidly abandoned these relationships, a process known as de-risking.

The retreat has been absolute and widespread. Barclays completed its century-long exit in 2022. Standard Chartered has divested subsidiaries across Angola, Cameroon, Gambia, Sierra Leone, and Zimbabwe between 2022 and 2025, and confirmed a full exit from Botswana in early 2026. In North Africa, Société Générale divested its Moroccan and Algerian interests in 2024-2025, while BNP Paribas shut down its South African investment arm in 2024.

This institutional pullback imposes a direct inefficiency tax on the African economy. Remittance fees to Sub-Saharan Africa average 8%–8.5%, nearly triple the UN target, a disparity identified by the United Nations Office of the Special Adviser on Africa (UN-OSAA) as a critical drain on regional development.

Intra-African corridors are even more punitive; records from the World Bank’s Remittance Prices Worldwide database show that sending $200 from South Africa to Malawi has historically incurred fees reaching 24%. Furthermore, the Chartered Institute of Bankers of Nigeria (CIBN) estimates that the reliance on external intermediaries in Europe or the US for intra-African settlement costs the continent $5 billion annually in fees and delays.

This crisis is compounded by macroeconomic shocks. Reports from Trendtype highlight that Egypt narrowly averted economic collapse in 2024 with an $8 billion IMF package following extreme currency overvaluation. Simultaneously, data from the Central Bank of Egypt indicates a 54.1% decline in Suez Canal transit receipts, further eroding foreign reserves.

Similarly, documentation from the U.S. Department of State reveals that Ethiopia’s 2024 transition to a floating exchange rate was a necessary response to a currency peg that had overvalued the Birr by more than 100%. For banks in these regions, the requirement to lock up precious USD in Nostro accounts is no longer just inefficient; it is a barrier to survival.

The architectural flaw: Messaging vs settlement

The fundamental technical flaw in the current system is its messaging-centric design. Systems like SWIFT do not move money; they send messages that say, “I owe you money”. The actual movement of value happens separately, days later, through the sequential updating of accounts across multiple intermediaries.

This multi-day settlement lag forces African banks to maintain massive pre-funded liquidity in Nostro accounts. If a bank in Nigeria lacks the specific USD liquidity to pre-fund its New York account, it cannot facilitate a trade payment to a Kenyan supplier, even if the bank is flush with local Naira. This liquidity trap ensures that capital, which could be used for local lending, is instead sitting idle in Western vaults.

Caption: The Correspondent Banking Bottleneck illustration

The paradigm shift: Packet switching for value

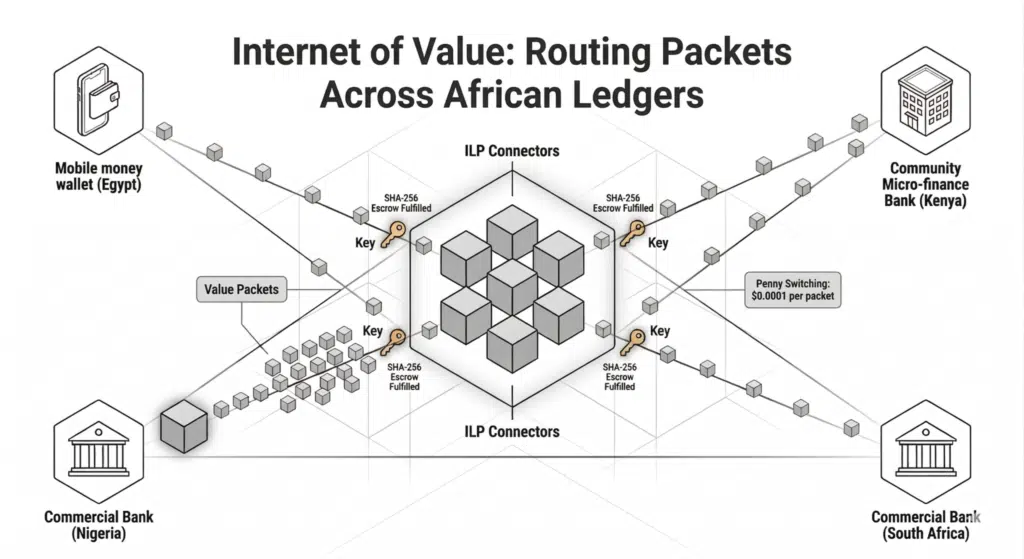

To fix Africa’s correspondent banking bottleneck, we must transition from messaging to switching. This is the proposition of the Interledger Protocol (ILP) and the Open Payments standard. While traditional banking resembles old circuit-switching telephone networks, ILP is modelled after the internet’s TCP/IP architecture.

ILP breaks a large payment into thousands of tiny data packets of value, a concept known as penny switching. Instead of sending a single $1,000 transfer that might fail and lock up capital, the system routes small packets across a web of independent connectors.

Each packet uses cryptographic escrow (specifically SHA-256 hashlocks) for atomic settlement. In this forward-and-backwards flow, the sender’s funds are debited when they receive cryptographic proof that the receiver has been paid.

This eliminates the free option problem, where a sender might exploit exchange rate shifts during a long settlement delay. Because these packets move instantly, connectors can operate with exponentially smaller pools of liquidity, freeing up the capital previously trapped in Nostro accounts.

Caption: Interledger Internet of Value illustration.

A new economic compact for the ecosystem

Transitioning to an Open Payments architecture isn’t just a technical upgrade, it’s a fundamental shift in the economics of African finance.

What does this mean for Banks?

For banking executives, Open Payments solves the most pressing commercial crisis of the de-risking era. As illustrated in the Comparative Flowchart, packet switching releases trapped liquidity from Western vaults. Instead of maintaining dead capital in New York or London to cover 3–5 day settlement lags, banks can settle intra-African trade in near real-time. Critically, tools like Rafiki act as an overlay, meaning banks don’t have to rip and replace their legacy core systems; they simply upgrade their rails to speak the universal language of the Interledger Protocol.

What does this mean for Regulators?

For central bank governors, this architecture addresses the $74.5 billion perception premium identified by the United Nations Development Programme (UNDP) as a cost of subjectivity that inflates borrowing costs for African nations. By domesticating intra-African payments via the Open Payments Standard, regulators can reduce the dangerous dependence on foreign currency for regional trade.

The Internet of Value provides unprecedented transparency; every tiny packet is cryptographically verified, curbing the informal underground flows that de-risking currently encourages. It moves the continent from digital islands to a unified, resilient financial ecosystem.

What does this mean for Payment Operators?

For mobile money providers and fintechs, Open Payments is a mandate for interoperability. As seen in the Interview of Value Diagram, disparate systems, such as Egypt’s mobile wallets and Nigeria’s bank ledgers, can finally interconnect without exclusive partnerships. Implementers like Fynbos in South Africa demonstrate that open standards can bridge these silos, converting once-invisible trade into a verifiable history. This lowers the barrier to entry, allowing innovators to compete on service quality rather than captive, closed-loop networks.

Regional analysis: Open payments progress

The adoption of the Open Payments standard in Africa is not a uniform wave but a series of regional breakthroughs led by fintech pioneers and academic hubs.

South Africa

South Africa remains the epicentre of Open Payments innovation. The University of Cape Town (UCT) Financial Innovation Hub has become a national leader, winning awards in 2025 for developing practical Open Payment solutions.

Projects like Team Direla have utilised the Interledger Protocol to enable low-income users and retail partners to transact without traditional point-of-sale hardware. Furthermore, the South African wallet provider Fynbos has successfully implemented Open Payments, enabling transfers between accounts across South Africa, Europe, and North America using user-friendly identifiers rather than bank codes.

West Africa

In West Africa, this shift is being spearheaded by Cool Lion Fi in Côte d’Ivoire. Recently recognised as a recipient of the Interledger Foundation’s Digital Financial Services grant, the company is working toward its goal of becoming a licensed node in the Interledger Network. Cool Lion Fi plans to leverage the Interledger Protocol (ILP) to facilitate cross-border business equipment loans for MSMEs across Francophone Africa.

By aiming to source capital from a global pool of fiat and crypto lenders and routing it via Interledger, they seek to bypass the high-friction correspondent banking hurdles that typically block small business credit. This approach treats digital infrastructure as compounding capital, converting once-invisible trade flows into a verifiable economic history that lowers risk for future lenders.

North Africa

In North Africa, the focus has shifted toward regulatory inclusion. The Interledger Foundation awarded the first Policy Activation Grant to the Alliance of Digital Finance and Fintech Associations (AllianceDFA) to lead initiatives in markets including Morocco and Egypt. This project specifically documents the successes of fintechs integrating the Open Payments standard to lobby for more inclusive governance in national payment systems.

East Africa

The future of Open Payments in East Africa is being built in the classroom. In 2025, the United States International University of Africa in Kenya was selected for the Interledger Nextgen Higher Education Grant Program. This program funds the development of interdisciplinary curricula focused on the Interledger Protocol and inclusive fintech, ensuring that the next generation of Kenyan students can build on open standards rather than proprietary, siloed legacy rails.

Pragmatic integration: Fixing the rails, Not the bank

Bank executives often hesitate to adopt new technology, fearing they must rip and replace their core banking systems. This is the beauty of Open Payments, it acts as an overlay.

Tools like Rafiki, an open-source financial software, manage the complexity of the Interledger network while providing a standardised API for developers. By using Rafiki, a bank can enable Payment Pointers (e.g., $babatunde.bank.ng) for its customers. When a payment is initiated, Rafiki resolves the pointer to a URL, discovers the Open Payments endpoints, and breaks the transaction into small packets for routing.

The Interledger Foundation currently supports this transition through grants of up to $250,000 for digital financial service providers, including banks and savings co-ops, to integrate Rafiki into their existing infrastructures. This allows legacy institutions to become active nodes on the Interledger network without abandoning their core ledgers.

The future: ecosystem over isolation

The correspondent banking model was designed for a world of physical ledgers and slow-moving maritime trade. It cannot keep pace with the velocity of a digital Africa. The $5 billion annual friction cost is not just a statistic; it is capital that could have built schools in Lagos, hospitals in Cairo, or fibre networks in Nairobi.

The technology for a connected, frictionless Africa exists. What is required is the strategic will to move from digital isolation to the Internet of Opportunity. Regulators and bank CEOs must recognise that interoperability does not destroy value; it redirects competition toward where it benefits consumers most: service quality and innovation.

The migration to stablecoins proves the demand from African users. The only question is which African country will move first to dismantle the digital islands and show the rest of the world the way.

About Author

Babatunde Hammed is a fintech operations strategist and a leading advocate for open payments and financial inclusion in Africa. Specialising in cross-border interoperability, he writes and speaks extensively on building the digital infrastructure needed to bridge financial gaps across the continent’s emerging markets.