African equities entered 2025 with caution. Inflation was still biting in several economies, currencies were volatile, and foreign investors remained selective about frontier exposure. By the end of the year, however, the picture looked very different. A handful of exchanges delivered exceptional gains, mid-sized markets posted solid advances, and a few smaller bourses struggled to stabilise.

Drawing on full-year quarterly averages from Kenya’s Capital Markets Authority (CMA), this review tracks how featured African exchanges performed from Q1 through Q4 2025. The comparison uses average quarterly market capitalisation in US dollars. However, that measure is not flawless. It reflects not only share-price movements, but also currency shifts, new listings, and changes in investor participation. Even so, it remains one of the clearest ways to assess how much value was created or erased across the year.

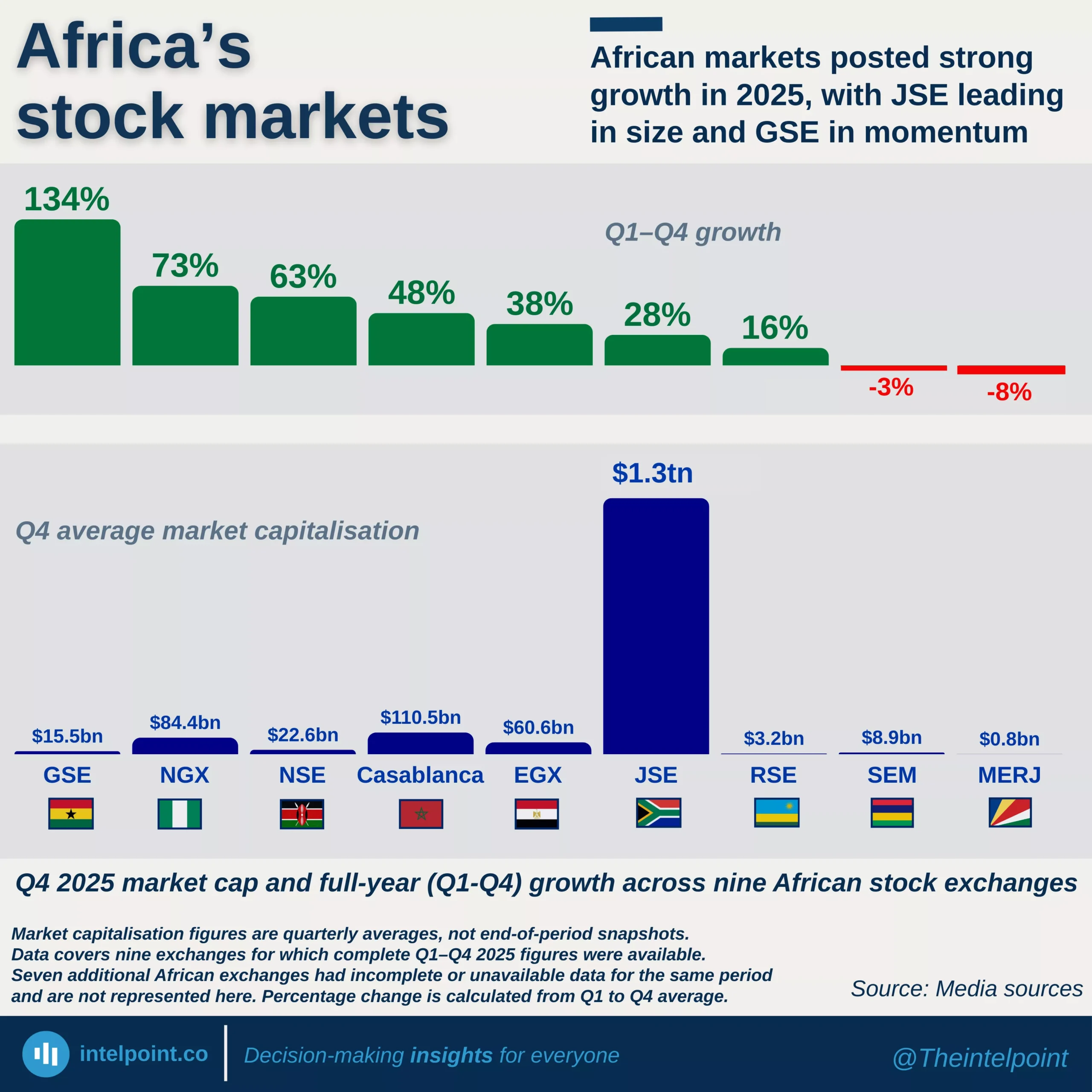

When the numbers are ranked from strongest to weakest Q1-to-Q4 performance, a striking pattern emerges: West Africa led the charge, East Africa gathered speed, North Africa maintained discipline, and a few offshore and island exchanges struggled to keep pace.

From mid-year momentum to full-year reality

In late 2025, Finance in Africa examined how selected exchanges performed between the second and third quarters. That mid-year analysis showed a clear inflection point that predicted the sustained trajectory of several markets, in both a positive and negative sense.

At the time, the data revealed a strong Q3 rebound across several markets. The Nigerian Exchange led the continent with a 25.83% quarter-on-quarter surge in market capitalisation between Q2 and Q3. The Nairobi Securities Exchange followed closely with a 23.39% jump. Morocco’s Bourse de Casablanca and the Egyptian Exchange both delivered double-digit gains, while smaller exchanges such as the Rwanda Stock Exchange and the Ghana Stock Exchange posted solid upward moves.

That earlier snapshot captured a moment when African equities appeared to be regaining confidence after a cautious first half. Inflation was easing in parts of the continent, currency volatility had moderated in key markets, and domestic institutional investors were stepping back in.

But a Q2-Q3 comparison tells only part of the story.

This full-year Q1-Q4 review reveals both convergence and divergence between the mid-year surge and the final outcome. Ghana’s outcome was the most surprising twist.

The standout performers of 2025

Ghana (+133.86%): A stunning repricing

The year’s most dramatic rally came from the Ghana Stock Exchange. Market capitalisation climbed from an average of $6.6 billion in Q1 to $15.5 billion in Q4, a 133.86% surge.

This was not incremental growth. It was a wholesale repricing of Ghanaian equities.

After weathering the turbulence of debt restructuring and macroeconomic strain in recent years, Ghana’s market appears to have benefited from renewed domestic confidence and improving investor sentiment. Banking and consumer-facing stocks drew particular interest, while local institutional investors, especially pension funds, increased their footprint.

The rebound suggests that markets can move quickly once confidence turns. Ghana’s 2025 performance was less about slow recovery and more about a sharp reset.

Nigeria (+73.06%): Scale meets momentum

Second place goes to the Nigerian Exchange, where average market capitalisation rose from $48.8 billion in Q1 to $84.4 billion in Q4.

Nigeria’s equity market combined structural reform, banking sector recapitalisation expectations, and renewed foreign interest. Currency stability, relative to prior turbulence, also helped valuations hold firm in dollar terms.

Quarter after quarter, capital flowed into financial services, energy-linked counters, and large industrial names. While the year did include bouts of volatility, the direction was broadly upward. Nigeria’s gain reflects both depth and breadth: it is one of the few African markets where liquidity, size, and reform momentum converged at the same time.

Kenya (+62.83%): Confidence returns to Nairobi

The Nairobi Securities Exchange delivered a 62.83% rise in average market capitalisation, climbing from $13.9 billion in Q1 to $22.6 billion in Q4.

Kenya’s recovery gathered pace mid-year and accelerated into Q4. Trading volumes improved, and key indices posted some of their strongest quarterly performances in years. Financial stocks and telecommunications counters played a central role in the rally.

Kenya’s story in 2025 was about regained credibility. After a period of subdued performance, the market reasserted itself as one of East Africa’s primary investment destinations.

Morocco (+47.83%): A steady performer

North Africa’s most consistent performer was the Bourse de Casablanca, where market capitalisation rose from $74.7 billion to $110.5 billion across the year.

Morocco’s nearly 48% gain was built on discipline rather than drama. Financials, industrials, and infrastructure-linked firms underpinned growth. Domestic institutional investors remained active, and policy continuity reinforced stability.

Unlike more volatile frontier exchanges, Casablanca’s rise felt measured. It reflected structural depth and relatively strong integration with European financial flows.

Egypt (+37.56%): Resilient under pressure

The Egyptian Exchange posted a 37.56% increase, moving from $44.1 billion in Q1 to $60.6 billion in Q4.

Egypt’s macroeconomic environment remained complex, with inflation and currency pressures shaping investor decisions. Yet equities showed resilience. Banking and real estate counters attracted renewed interest, supported by reform efforts and international financial engagement.

While the growth rate lagged behind West African peers, Egypt maintained its status as one of the continent’s most liquid markets. Stability, even amid macro headwinds, remains a key strength.

South Africa (+27.63%): Large, liquid, and measured

Africa’s largest exchange, the Johannesburg Stock Exchange, expanded from $1.02 trillion in Q1 to $1.30 trillion in Q4, representing a 27.63% gain.

On percentage terms, South Africa’s performance sits mid-table. In absolute terms, however, the value added was enormous. Mining, financials, and renewable energy-linked stocks supported gains.

The JSE’s year was not explosive. It was steady. Its scale continues to anchor African capital markets, and its liquidity offers depth that smaller exchanges cannot easily replicate.

Rwanda (+15.54%): Quiet but consistent

The Rwanda Stock Exchange advanced from $2.74 billion to $3.17 billion across the year.

Rwanda’s market remains small, but its upward trajectory has been consistent. Gains reflect stable corporate earnings and regulatory credibility. For investors seeking lower volatility exposure within the region, Rwanda continues to stand out.

The laggards

Mauritius (-2.61%): Flat to negative

The Stock Exchange of Mauritius ended 2025 slightly below its starting point, slipping 2.61% from $9.18 billion in Q1 to $8.94 billion I Q4 2025.

Mauritius retains its reputation as a regional financial hub, but growth in listed equity value was muted. Limited new listings and cautious investor positioning likely contributed to the mild contraction.

Seychelles (-8.02%): Offshore volatility

The MERJ Exchange Limited declined 8.02% over the year, falling from $824 million to $758 million.

As one of Africa’s more digital-forward exchanges, MERJ plays a niche role connecting offshore capital with African assets. Its negative performance in 2025 highlights the sensitivity of smaller, specialised exchanges to shifts in global risk appetite.

| Growth performance of African stock exchanges from Q1 to Q4 2025 | ||||||

| Stock Exchange | Country | Q1 Avg | Q2 Avg | Q3 Avg | Q4 Avg | % Change Q1-Q4 |

| Ghana Stock Exchange (GSE) | Ghana | 6,617.85 | 11,983.70 | 13,237.00 | 15,476.95 | +133.86% |

| Nigerian Exchange (NGX) | Nigeria | 48,782.59 | 60,143.70 | 75,677.00 | 84,418.36 | +73.06% |

| Nairobi Securities Exchange (NSE) | Kenya | 13,854.41 | 16,786.30 | 20,712.00 | 22,557.28 | +62.83% |

| Bourse de Casablanca | Morocco | 74,729.70 | 101,302.00 | 113,387.00 | 110,469.49 | +47.83% |

| Egyptian Exchange (EGX) | Egypt | 44,083.54 | 46,032.30 | 51,352.00 | 60,643.08 | +37.56% |

| Johannesburg Stock Exchange (JSE) | South Africa | 1,022,070.85 | 1,110,205.30 | 1,216,942.70 | 1,304,516.56 | +27.63% |

| Rwanda Stock Exchange (RSE) | Rwanda | 2,741.10 | 2,710.70 | 2,995.00 | 3,167.29 | +15.54% |

| Stock Exchange of Mauritius (SEM) | Mauritius | 9,183.42 | 9,164.00 | 9,231.30 | 8,944.25 | -2.61% |

| MERJ Exchange Limited | Seychelles | 824.16 | 790.30 | 833.30 | 758.02 | -8.02% |

*All figures represent quarterly average market capitalisation in USD ($) millions.

The transparency gap

Several African exchanges were excluded from full-year comparison due to incomplete or inconsistent reporting. The following markets published partial or missing quarterly data across 2025:

- Botswana Stock Exchange

- Angolan Securities Exchange (BODIVA)

- Lusaka Securities Exchange (Zambia)

- Namibian Stock Exchange

- Dar es Salaam Stock Exchange (Tanzania)

- Tunis Stock Exchange (Tunisia)

- Bourse Régionale des Valeurs Mobilières (Benin, Burkina Faso, Cote D’ivoire, Guinea-Bissau, Mali, Niger, Senegal, Togo)

These gaps matter. Investors rely on timely, transparent information to allocate capital confidently. Inconsistent reporting does not necessarily reflect weak performance, but it does limit visibility and comparability. As Africa’s capital markets deepen, data transparency will remain a defining issue.

| African stock exchanges with missing or incomplete 2025 Data | ||||||

| Stock Exchange | Country / Region | Q1 Avg | Q2 Avg | Q3 Avg | Q4 Avg | Nature of Data Gap |

| Botswana Stock Exchange | Botswana | Unavailable | Unavailable | Unavailable | Unavailable | No full capitalisation data published |

| Angolan Securities Exchange (BODIVA) | Angola | Unavailable | Unavailable | Unavailable | Unavailable | No quarterly capitalisation data published |

| Lusaka Securities Exchange | Zambia | Unavailable | Incomplete | Incomplete | Unavailable | Partial reporting; inconsistent quarterly averages |

| Namibian Stock Exchange | Namibia | Incomplete | Incomplete | 2,896 | Unavailable | Partial figures only; inconsistent reporting |

| Dar es Salaam Stock Exchange | Tanzania | Incomplete | Incomplete | Unavailable | Unavailable | No full quarterly averages available |

| Bourse Régionale des Valeurs Mobilières (BRVM) | WAEMU Region (8 countries) | Unavailable | Unavailable | 21,768.70 | Unavailable | Only Q3 data available |

| Tunis Stock Exchange | Tunisia | 8,378.71 | 10,037.30 | Incomplete | 11,501.85 | Missing Q3 data prevents full-year comparison |

Lessons from 2025

Three core themes shaped the year and were instrumental in equity outcomes for African markets.

- Reform rewarded markets: Nigeria and Ghana, both navigating structural adjustments, saw outsized gains once investor confidence returned.

- The importance of domestic liquidity deepened: Morocco and South Africa demonstrated how strong local institutional bases can sustain steady growth even during global uncertainty.

- Size was not equal to destiny: Smaller exchanges such as Rwanda outperformed some larger peers on a percentage basis, proving that disciplined growth can trump scale.

Outlook for 2026: Momentum meets caution

As African markets step into 2026, the early signals suggest that the optimism of 2025 has not faded. Several exchanges that ended last year strongly have begun the new one, even before Q1 ends, with renewed investor interest, particularly across West and East Africa.

The Nigerian Exchange

The Nigerian Exchange is one of the clearest examples. The market entered 2026 with strong momentum following its sharp expansion in 2025, with a value jump of 125% according to the Securities and Exchange Commission (SEC). Market capitalisation has climbed from about ₦55 trillion in April 2024 to over ₦126 trillion (about $91 billion) in early March, 2026. Also, the benchmark All-Share Index (ASI) rose sharply by 16.6% to close February at 192,826.78 points from 165,370.40 points in January.

The rally reflects a mix of improving foreign participation, stronger domestic institutional activity, and relative currency stability compared with the turbulence seen in earlier reform periods.

Commenting on the significance of Nigeria’s impressive market capitalisation figures for the economy and the role of liquidity, the Director-General of the SEC, Emomotimi Agama, stated: “Our contribution to GDP has moved from 13% to 33%. These are impressive figures, but they tell only part of the story…A capital market is often described as the barometer of an economy’s health. But for that barometer to be accurate, the market must be more than just large—it must be liquid.”

Dar es Salaam Stock Exchange (Tanzania)

East Africa has also begun the year on a positive note. The Dar es Salaam Stock Exchange has emerged as one of the continent’s early outperformers in 2026, with analysts reporting an extension of year-to-date gains to 40.65% as investor appetite broadens beyond the largest African markets. Tanzania’s rise reflects growing interest in mid-sized frontier exchanges that combine relatively stable macroeconomic environments with expanding corporate sectors.

Ghana Stock Exchange

The Ghana Stock Exchange, which delivered the strongest performance among tracked exchanges in 2025, has also opened the new year with modest gains. After a year in which market capitalisation more than doubled, the early months of 2026 appear to reflect consolidation rather than another immediate surge. For investors, this slower start is not necessarily negative; it suggests the market may be digesting last year’s dramatic repricing.

Meanwhile, North African markets such as the Bourse de Casablanca and the Egyptian Exchange are likely to remain steady rather than explosive performers.

Maintenance or growth?

The broad trajectory is encouraging. After years of uneven performance, 2025 showed that African equity markets can deliver powerful returns when macro conditions align with policy clarity and investor confidence.

The key question for 2026 is not whether growth is possible. It is whether the reforms, stability, and liquidity that powered 2025 can be sustained.

If they are, Africa’s capital markets may be entering a more mature phase, one defined not by sporadic rallies, but by deeper, more durable expansion.

N.B: Figures originally reported in Nigerian naira and converted using the average exchange rate of ₦1386/ $1 as of Thursday, March 5, 2026.