Across Africa, cement is more than a construction input; it is a proxy for ambition. Wherever new housing estates rise on city fringes, and where governments tout industrial corridors, cement is never far from the story. In Nigeria, the craze with cement roads ensures that when highways stretch across vast lands, cement is part of the story.

From Nigeria to Egypt, from Kenya to South Africa, the continent’s cement heavyweights sit at the centre of Africa’s infrastructure push.

In Nigeria, cement makers such as Dangote Cement and BUA Cement rank among the largest companies on the Nigerian Exchange, reflecting the strategic weight the sector carries in Africa’s biggest economy.

Cement demand remains one of the most reliable indicators of industrial momentum: it signals public infrastructure spending, private real estate cycles, and the pace of urbanisation. Bridges, dams, residential towers, and highways all leave a cement trail in their wake.

Yet, beneath this continental growth narrative lies a more complex financial picture. A review of the 2024 financial statements of selected cement companies across North, East, South, and West Africa reveals a divergence in profitability and resilience.

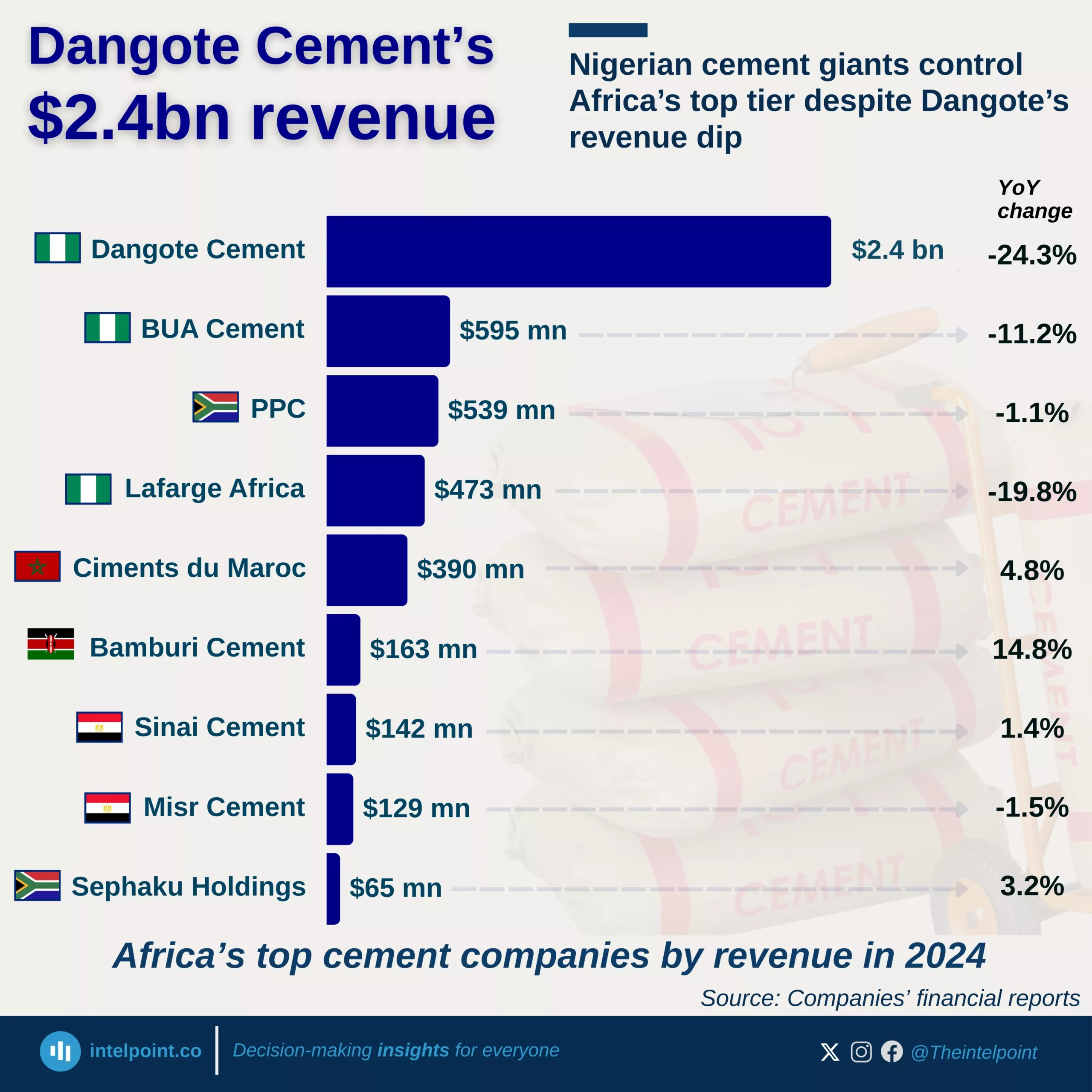

While capacity is spread across the continent, profits are not. Nigerian cement makers, despite currency headwinds, remain among the most profitable operators, recording the highest cumulative margins across core operations.

The scale of Africa’s cement giants

Nigeria’s Dangote dominates in West Africa and beyond

Africa’s largest cement producer is Nigeria’s Dangote Cement, with an installed production capacity of 52.5 million tonnes per annum (mtpa) across 10 African countries.

Of this, 35 million tonnes are domiciled in Nigeria. However, scale does not always translate to full utilisation. In 2024, Dangote produced 28.7 million tonnes, implying a 52.8 per cent capacity utilisation rate, a reminder of uneven demand conditions across markets.

Despite softer volumes and currency pressures, Dangote Cement remains the continent’s largest revenue generator. In 2024, it posted net sales of $2.4 billion, down from $3.2 billion in 2023. Its Nigerian operations alone accounted for $1.5 billion of that figure, underlining the domestic market’s centrality to group performance.

Beyond Nigeria, Dangote operates in Ethiopia, Zambia, Senegal, Guinea, DR Congo, Mozambique, Madagascar, Tanzania, and the Republic of Congo, while exporting cement from Nigeria to the Benin Republic, Ghana, Liberia, Burkina Faso, Niger, Chad, and Togo. Its footprint mirrors Africa’s trade corridors.

Within West Africa, Nigeria’s total cement production capacity stands at roughly 65 million tonnes. BUA Cement controls 17 million tonnes, while Lafarge Africa holds 10.5 million tonnes. In 2024, BUA recorded net sales of $573 million, while Lafarge Africa generated $455 million.

Dangote extends lead into East Africa

Part of Dangote Cement’s empire is seen in Tanzania, where the company is the largest producer by capacity in East Africa. With a 3 million tonnes per annum factory in Mtwara, Tanzania, Dangote Cement Tanzania edges out Tanzania Portland Cement Company (TPCC), which owns a 2 MTPA plant in Dar es Salaam.

In terms of revenue, Dangote Cement generated $176 million in revenue, just slightly higher than the $174 million generated by TPCC.

For neighbouring Kenya, Bamburi Cement is the country’s largest producer, with a 1.8 million tonne annual capacity. It generated $163 million in revenue in 2024. nearly seven times the $24 million reported by East Portland Cement Company. The disparity reflects both scale advantages and operational headwinds within Kenya’s cement market.

PPC dominates in Southern Africa

Unlike East Africa, there is a single dominant player in South Africa. PPC Limited (Pretoria Portland Cement) is the region’s dominant player, with plants in South Africa, Zimbabwe, and Botswana and a combined annual capacity of 11.6 million tonnes.

Sephaku Holdings, another listed operator, has an integrated capacity of 1.9 million tonnes, including a 1.8 million tonne clinker plant and a grinding plant co-owned with Dangote Cement.

In 2024, PPC generated $538 million in revenue, making it one of Africa’s top revenue earners behind Dangote Cement and BUA Cement. Sephaku posted about $64 million.

There’s slightly stiffer competition in North Africa

North Africa’s market is capacity-heavy. Egypt’s National Company for Cement Beni Suef and Heidelberg Materials (Suez Cement) both boast 12 million tonnes of installed capacity. Meanwhile, in Morocco, Ciments du Maroc leads with 8 million tonnes and reported $389 million in net sales in 2024, the highest in the country. Due to its unlisted status, National Company for Cement Beni Suef’s 2024 revenue remains unverifiable.

Margins and profitability

Core strength masks currency strain in Nigeria

In West Africa, profitability remains anchored in Nigeria, even as currency volatility distorts headline figures. Dangote Cement posted net income of $342 million in 2024 (₦503 billion in constant currency terms), a sharp decline from $717 million in 2023. The drop was largely driven by the 53 per cent depreciation of the naira, which significantly eroded earnings when translated into dollars.

Yet beneath the currency effect lies a more resilient domestic story. Dangote’s Nigerian operations generated $805 million in net income in 2024, only slightly below the $807 million recorded a year earlier. While pan-African subsidiaries dragged consolidated earnings lower, the Nigerian core business remained strongly profitable, posting a remarkable 54 per cent margin.

Other Nigerian players delivered more modest but stable results. Lafarge Africa recorded $68 million in net income with a 14.4 per cent profit margin, slightly ahead of Dangote’s consolidated 14.1 per cent margin. BUA Cement posted $50 million (₦73.9 billion) in net income and an 8.4 per cent margin, reflecting tighter cost pressures within the domestic market.

Egypt’s asset-driven margins, Morocco’s operational discipline

In North Africa, profitability tells a more nuanced story. Egypt’s Sinai Cement delivered $67.7 million in net income on revenues of $142 million, the highest revenue among Egypt’s listed cement producers. Its headline 48% profit margin led the continent. However, much of that performance was driven by investment asset sales rather than core cement operations.

Similarly, Misr Cement Beni Suef generated $22 million in net income and posted a strong 26% margin, underscoring Egypt’s ability to produce high reported margins, though often influenced by non-operational gains. Misr Cement Qena added $6 million in net income.

In contrast, Morocco’s Ciments du Maroc demonstrated steadier operational performance. The company recorded $90.5 million in net income in 2024, an 8 per cent dip from the previous year, while maintaining a solid 23 per cent profit margin, one of the strongest among companies driven primarily by core operations rather than asset disposals.

Zimbabwe comes to the aid of PPC

In Southern Africa, profitability was comparatively thinner but strategically supported by regional diversification. PPC Limited posted $25.4 million in net income in 2024. Notably, its Zimbabwean subsidiary contributed $16.7 million, providing a critical earnings cushion amid softer domestic conditions in South Africa.

Sephaku Holdings reported a 7.6 per cent profit margin, reflecting tighter spreads in a more competitive market environment. While revenues remain significant, Southern Africa’s cement makers appear to operate in a more margin-constrained setting compared to their West and North African counterparts.

The continental divide

The numbers suggest a layered story. Capacity is widely distributed across Africa, but sustainable profitability remains concentrated in markets with scale, pricing power, and operational efficiency, particularly Nigeria and Morocco.

In Egypt and Kenya, headline margins were flattered by non-operational gains. In Southern Africa, regional diversification provided buffers against domestic slowdowns.

Ultimately, Africa’s cement heavyweights are navigating divergent macroeconomic climates, currency regimes, and demand cycles. Cement may be a commodity, but in Africa, profitability is anything but uniform.