In 2023, Ghana’s economy was in distress. The Ghanaian cedi had lost much of its value, inflation was running hot, and a sovereign debt crisis had forced the government into restructuring. For investors, the story was simple: stay away.

By 2025, that story had flipped dramatically.

The Ghana Stock Exchange not only recovered; it emerged as Africa’s best-performing bourse, percentage-wise, delivering a rally that surprised even seasoned frontier market investors. What changed was not just sentiment. It was structured: a coordinated reset of Ghana’s external position, fiscal credibility, and financial system.

At the centre of the turnaround was gold. But the real story goes beyond the fact that gold prices rose. It extended to the reality that Ghana restructured how gold flows through its economy, and used that shift to stabilise everything else.

How a commodity caused a windfall

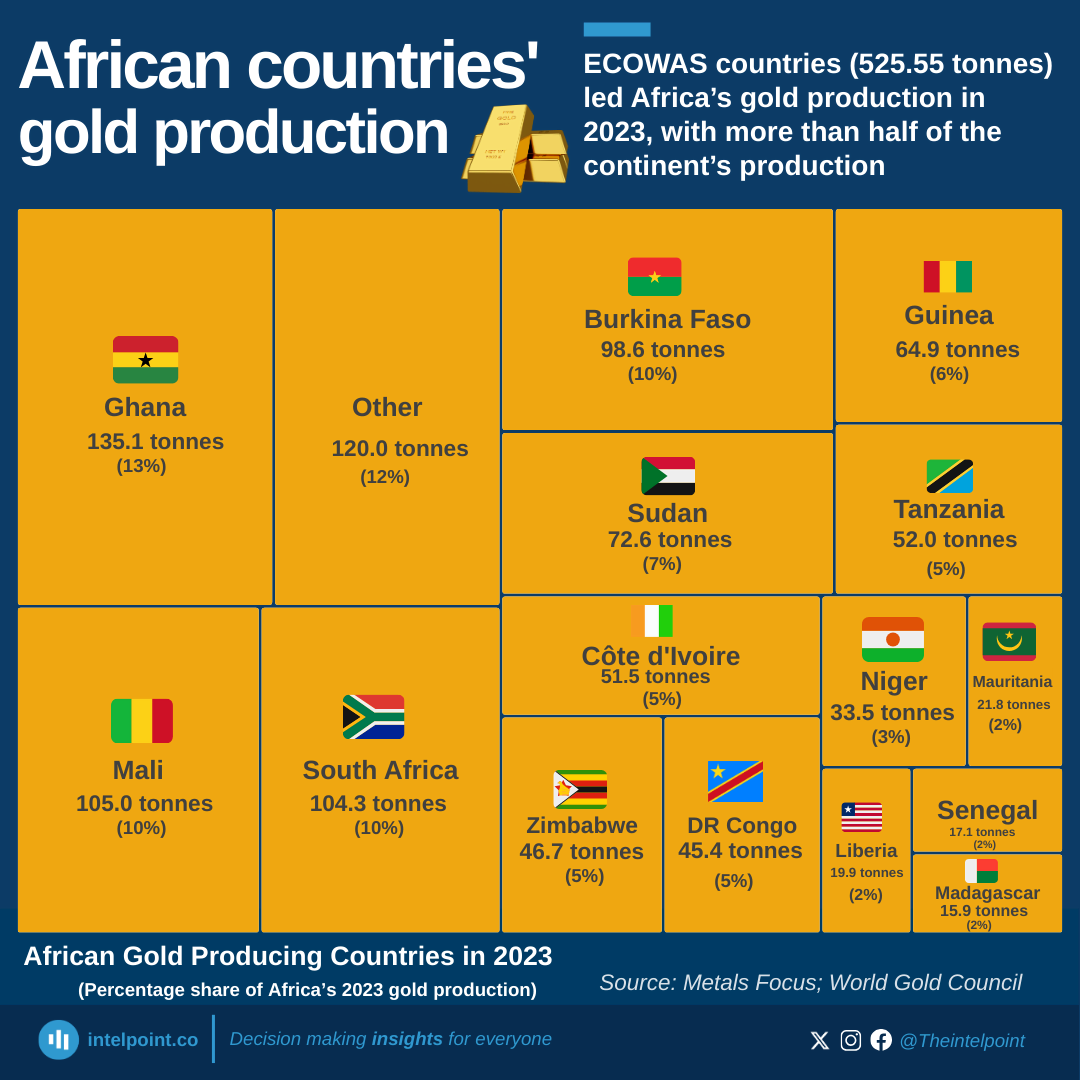

Ghana has always been exposed to gold. As Africa’s largest producer, its export earnings have long been tied to global prices. Although the price environment was a strong factor, what really drove the change between 2024 and 2025 was the country’s ability to capture and retain value.

Three developments stand out.

The price of gold

First, global gold prices surged to historic highs, averaging about $2,400 per ounce in 2024 before accelerating into a record-breaking 2025, where prices averaged above $3,400 and climbed past $4,300 per ounce as gains accelerated sharply in the final quarter, driven by geopolitical uncertainty and sustained central bank demand. The World Gold Council puts the full-year return at about 67% year-on-year.

In its Gold Outlook 2026 report, the council stated: “Gold has experienced a remarkable 2025, achieving over 50 all-time highs and returning over 60%. This performance has been supported by a combination of heightened geopolitical and economic uncertainty, a weaker US dollar, and positive price momentum.”

For Ghana, this translated into a sharp increase in export receipts. Gold export earnings rose from about $6.6 billion in 2022 to $7.6 billion in 2023, before surging to roughly $10–11 billion in 2024 and then nearly doubling again to around $20 billion in 2025, strengthening the country’s current account position and driving a rare surplus.

To better understand the scale of the turnaround caused by this commodity, Ghana’s total revenue from exports was an incremental $31.1 billion in 2025, rising from $19.1 billion in 2024. Of that export figure, gold generated $20.9 billion, cementing it as the country’s historic leading export, ahead of other natural exports like cocoa and oil.

The structure from specific reforms in 2025 was largely responsible for this, particularly artisanal and small-scale gold mining which was formalised and regulated by the Ghana Gold Board (GoldBod).

Resilient production

Second, production remained resilient. Ghana’s gold output reached roughly 4.0 million ounces in 2023 and expanded further to around 4.8–4.9 million ounces in 2024, reflecting a nearly 20% increase in annual output.

Large-scale operators like Newmont Corporation and AngloGold Ashanti, as well as a fast-growing artisanal and small-scale mining segment, now accounting for close to 40% of total production, further advanced this growth. This ensured that Ghana fully captured the upside from rising prices rather than being constrained by volume.

As Michael Edem Akafia, Vice President for External Affairs at Gold Fields, noted, the sector saw a “70.1% increase in attributable output… reflecting recent support measures and higher gold prices,” underscoring how policy and price dynamics combined to lift production.

Policy-driven transformation

Third, and most critically, policy changes altered the flow of those earnings.

The government maintained its headline gold royalty rate at 5%, but the more consequential shift came from how it captured value across the supply chain. Authorities moved to centralize gold purchases and exports through the state-backed Ghana Gold Board, established in 2025 as the sole buyer and exporter of gold from artisanal and small-scale miners.

This was complemented by the Bank of Ghana’s Domestic Gold Purchase Programme (DGPP), under which official gold reserves rose from 8.77 tonnes in 2022 to about 30.8 tonnes by early 2025, and reaching around 38.0 tonnes by October, 2025. The impact was immediate: GoldBod alone helped generate roughly $8 billion in foreign exchange inflows, while formal exports surged, including about 56 tonnes of gold, worth $5 billion which would have otherwise been lost to smuggling, shipped in just the first five months of 2025.

Speaking on the role of central banks, Andrew Naylor, Head of Middle East and Public Policy at the World Gold Council, explained, “Central banks remain a pivotal force in shaping global gold demand, providing both stability and strategic direction for the market…Our latest Central Bank Gold Survey (2025) found that 95% of the central banks surveyed expect global official gold reserves to increase over the next 12 months, the highest level of optimism recorded in our series”

These measures from Bank of Ghana and GoldBod targeted long-standing leakages from smuggling and informal trading by incentivizing miners to sell at near-market prices through official channels. Smuggling and informal trading had cost Ghana an estimated $11.4 billion between 2019 and 2023, according to Reuters. The result of the new measures was a structural shift in how gold revenues were captured, with a significantly larger share of export proceeds now flowing back into the formal financial system.

The combined effect was more structural than incremental. For the first time in years, Ghana was not just exporting gold. It was retaining the liquidity generated by it.

The external constraint fix: From export earnings to reserves

Most developing markets aren’t struggling with economic growth per se; they’re struggling to find the foreign exchange they need to keep moving.

Ghana’s crisis across 2022 and 2023 illustrates this clearly. The country faced a severe balance-of-payments shortfall, with gross international reserves falling sharply from about $9.7 billion in 2021 to $6.2 billion by the end of 2022, and dropping further to around $5.9 billion by February 2023, equivalent to less than three months of import cover.

The shortage of foreign exchange triggered intense pressure on the Ghanaian cedi, which depreciated by about 30% against the US dollar in 2022 alone, with additional losses of roughly 20–25% during 2023. This sharp depreciation fed directly into inflation. Consumer prices surged, with inflation peaking at around 54% in December 2022 before easing but still remaining elevated at about 23% by the end of 2023.

As the currency weakened and inflation accelerated, confidence in the economy deteriorated. Ghana experienced portfolio outflows, reduced foreign investment, and loss of access to international capital markets, all of which intensified pressure on reserves and reinforced the cycle of instability.

The gold windfall, combined with tighter controls on export proceeds, began to reverse that cycle.

The effect of GoldBod and the Bank of Ghana’s Domestic Gold Purchase Programme’s efforts caused a dramatic shift. Gross international reserves rose from about $5.9 billion at the end of 2023 to roughly $8.98 billion by the end of 2024, and continued climbing to between $10 billion and $11 billion through 2025, according to Bank of Ghana data.

This pushed import cover from around 2.7 months in 2023 to about 4.0 months by end-2024, and further to roughly 4.5–4.8 months during 2025, comfortably above the three-month benchmark often used for external stability.

This mattered not just for optics, but for market function. A country with rising reserves can:

- Intervene more credibly in currency markets, stabilizing exchange rates.

- Smooth volatility, protecting both importers and exporters.

- Signal its ability to meet external obligations, reassuring investors that their capital is safe.

By 2025, Ghana had moved from scarcity to relative sufficiency. The pressure on the currency eased, and the economy regained the breathing room necessary for a sustained equity market recovery.

How the IMF helped rebuild credibility

While internal adjustments created a transformative effect, an external factor also played a pivotal role in Ghana’s rebound.

Ghana’s engagement with the International Monetary Fund provided a structured path out of crisis at a time when investor trust had collapsed. In May 2023, the IMF approved a $3 billion Extended Credit Facility, unlocking immediate financing and anchoring a broader reform programme.

Debt restructuring was central to that effort. Ghana completed its domestic debt exchange in 2023 and restructured its Eurobonds in 2024, a process expected to reduce debt by about $4.7 billion and deliver roughly $4.4 billion in cash flow relief through 2026.

The impact showed up quickly in the numbers. Public debt, which had peaked at over 85% of GDP in 2022, began to decline steadily, falling toward the 60–70% range by 2024–2025 as fiscal consolidation took hold.

At the same time, the IMF programme enforced discipline on both spending and monetary policy. Ghana moved toward a primary fiscal surplus target of about 1.5% of GDP, while inflation began to ease and macro conditions stabilized.

The rules were becoming predictable again. And this increased investor optimism to take risks.

A question of durability

It is tempting to attribute Ghana’s market performance to a favourable commodity cycle. That explanation is incomplete.

What set Ghana apart in 2025 was not just that gold prices rose. It was that the country captured more of that value, retained it within the financial system, and used it to stabilize the macroeconomy.

The capture-retain-stabilize sequence restored confidence. And in markets like Ghana’s, confidence is everything.

The rally, in that sense, was not accidental. It was engineered.

Whether it continues will depend on if that discipline proves durable in an increasingly volatile financial environment.