Nigerian stock market weekly report

Looking back to plan ahead – Monday, 14 July 2025

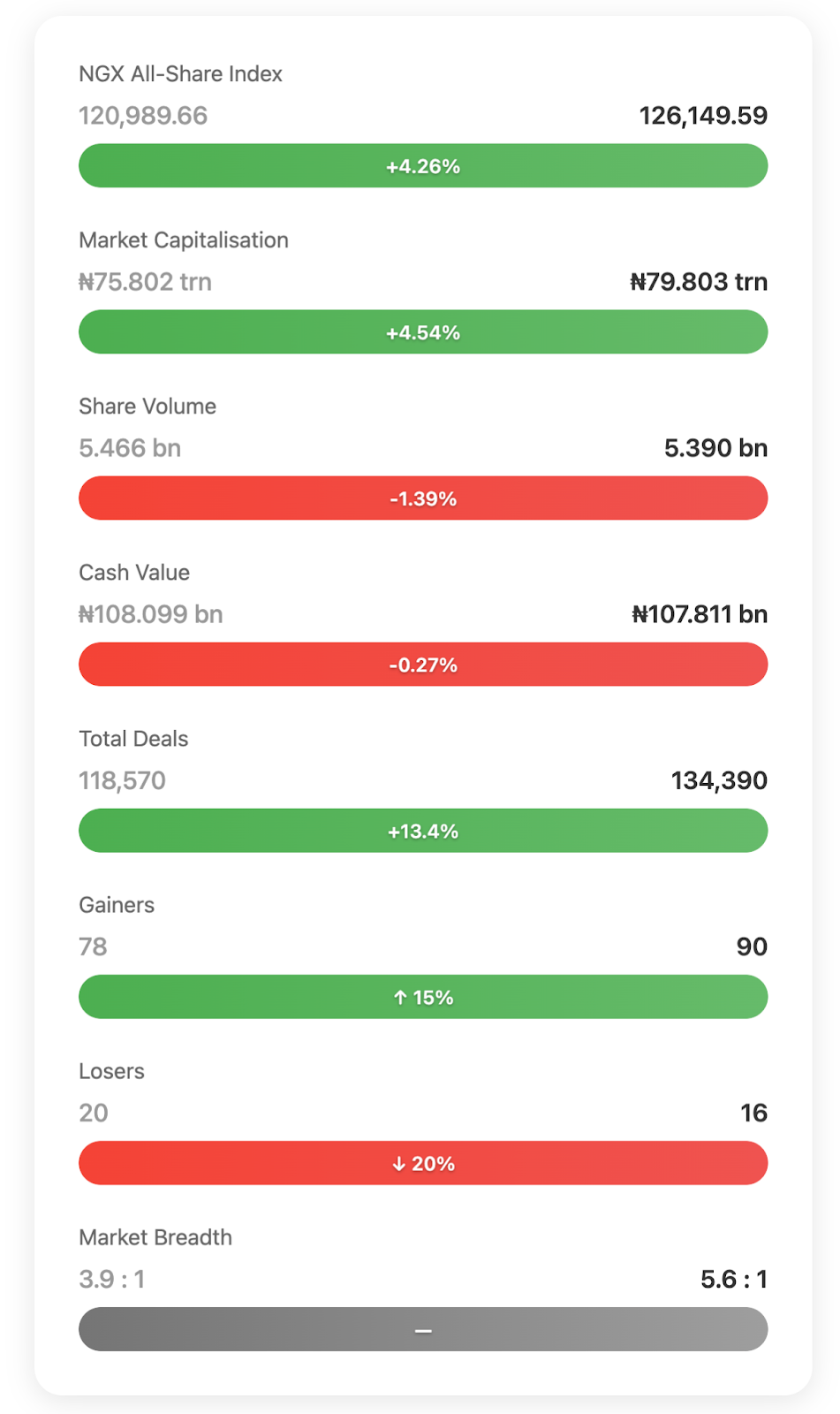

Here’s what happened last week, and why it matters for the trading desk this morning. From July 7 to 11, the NGX All-Share Index exploded 4.26% higher, reaching an all-time closing high of 126,149.59 points, its best weekly percentage gain since mid-March.

Market capitalisation crossed the ₦79.8 trillion mark, adding roughly ₦3.46 trillion in paper wealth. However, the headline rally only provides a partial picture.

Breadth was breathtaking: 90 gainers versus just 16 losers, a 5.6-to-1 advance/decline spread that eclipses anything we’ve seen this quarter. Under the bonnet, bank and insurance stocks ripped double digits, while oil and gas names stalled, signaling a sharp risk-on rotation toward financial beta and dividend yield. Liquidity held steady (₦107.8 billion in cash value) even as share volume eased 1%, telling us buyers paid up for quality rather than chasing pennies.

As we begin the week of 14 July, the index sits less than two sessions away from the psychologically weighty 127k handle. Momentum is fierce, but overhead supply at new-high territory and looming Q2 results could turn this sprint into a hurdles race.

I have included my stock market report for week 2 of July 2025 here if you need more context.

Key market metrics from last week

Market analysis narrative

Here’s what really caught our attention. A 4%+ index surge paired with flat turnover value means buyers paid materially higher prices for roughly the same naira outlay, classic price-led breakout behaviour. Leadership was unambiguous:

- The Banking Index rose 12.49%, its biggest weekly pop of 2025, on the back of GTCO’s oversubscribed public-offer listing and aggressive blocks in Zenith and Access.

- The Insurance Index increased by 13.83%, as the lowest price-to-book cohort attracted dividend hunters in anticipation of half-year numbers.

- The Premium Index increased by 8.14%, indicating that the blue-chip basket has finally participated after several weeks of underperformance.

Meanwhile, the Oil & Gas Index slipped 0.72%, weighed by profit-taking in Oando. The divergence tells us rotational, not indiscriminate, buying: investors cycled out of energy beta and into financials, where net interest income is expected to jump with rising yields.

Daily tape action reinforced the shift. Thursday’s ₦27.7 billion value spike coincided with a 70/10 breadth crush, with institutional money marking positions ahead of Friday’s MSCI basket review rumors. Friday kept the pressure on, posting the week’s highest deal count (33,399) and cash value (₦30.55 billion), confirming strong hands were still active into the close.

Volume composition matters too. Financial Services printed 56% of shares and 52% of cash, but Oil & Gas dropped to 7.5% of naira turnover, its lightest share since February. Translation: Smart money is betting next week’s bank earnings will justify 15-20% YTD multiple expansion while waiting for fresh catalysts in energy.

Winners & Losers Analysis

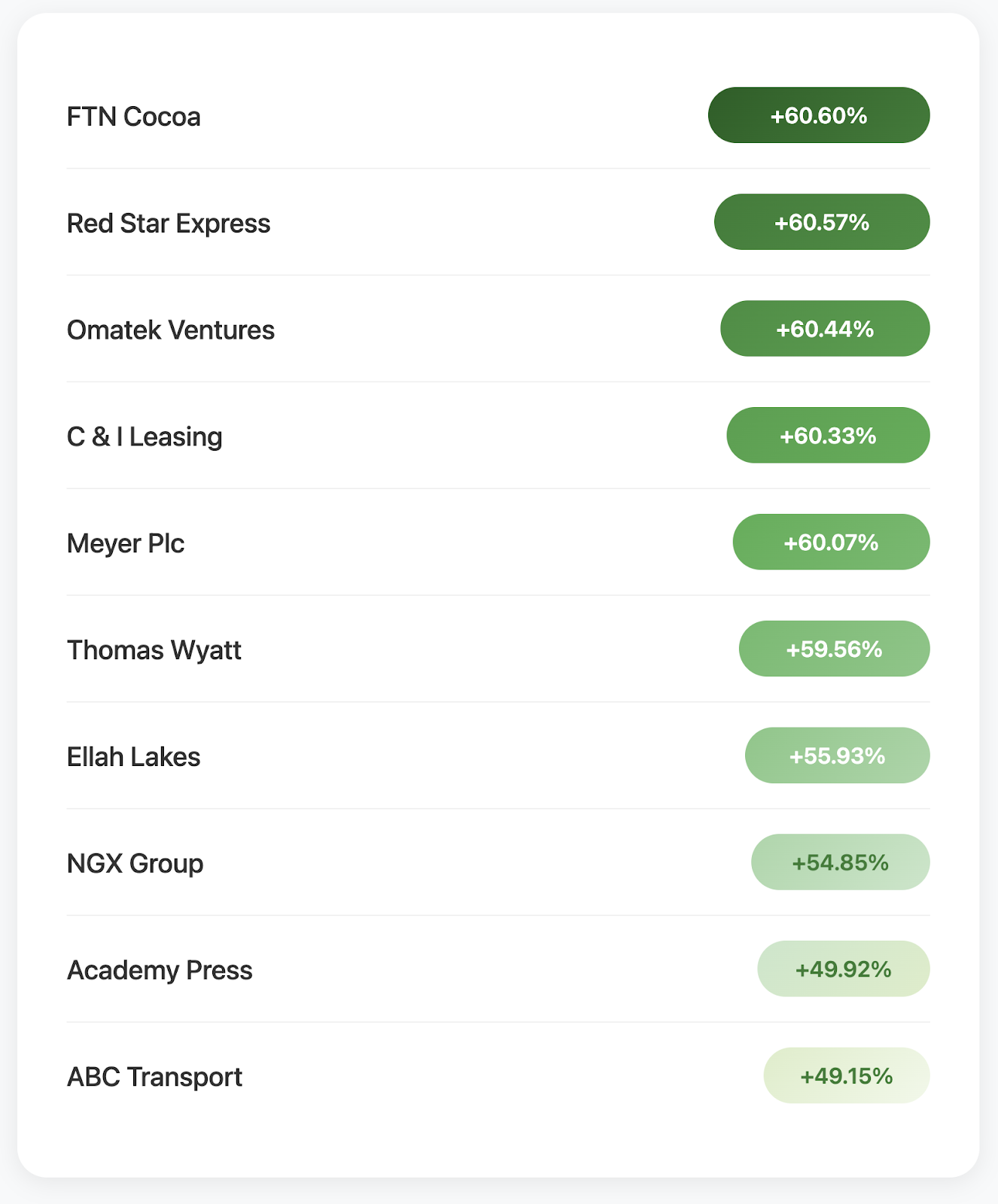

Top 10 Gainers

What it means: Small-to-mid caps account for eight of the ten winners, indicating a vigorous pursuit of risk. Notice the logistics (Red Star, ABC), agro-allied (FTN Cocoa, Ellah Lakes), and service-leasing (C & I) theme; investors are bidding up pockets of secular demand rather than any single sector momentum.

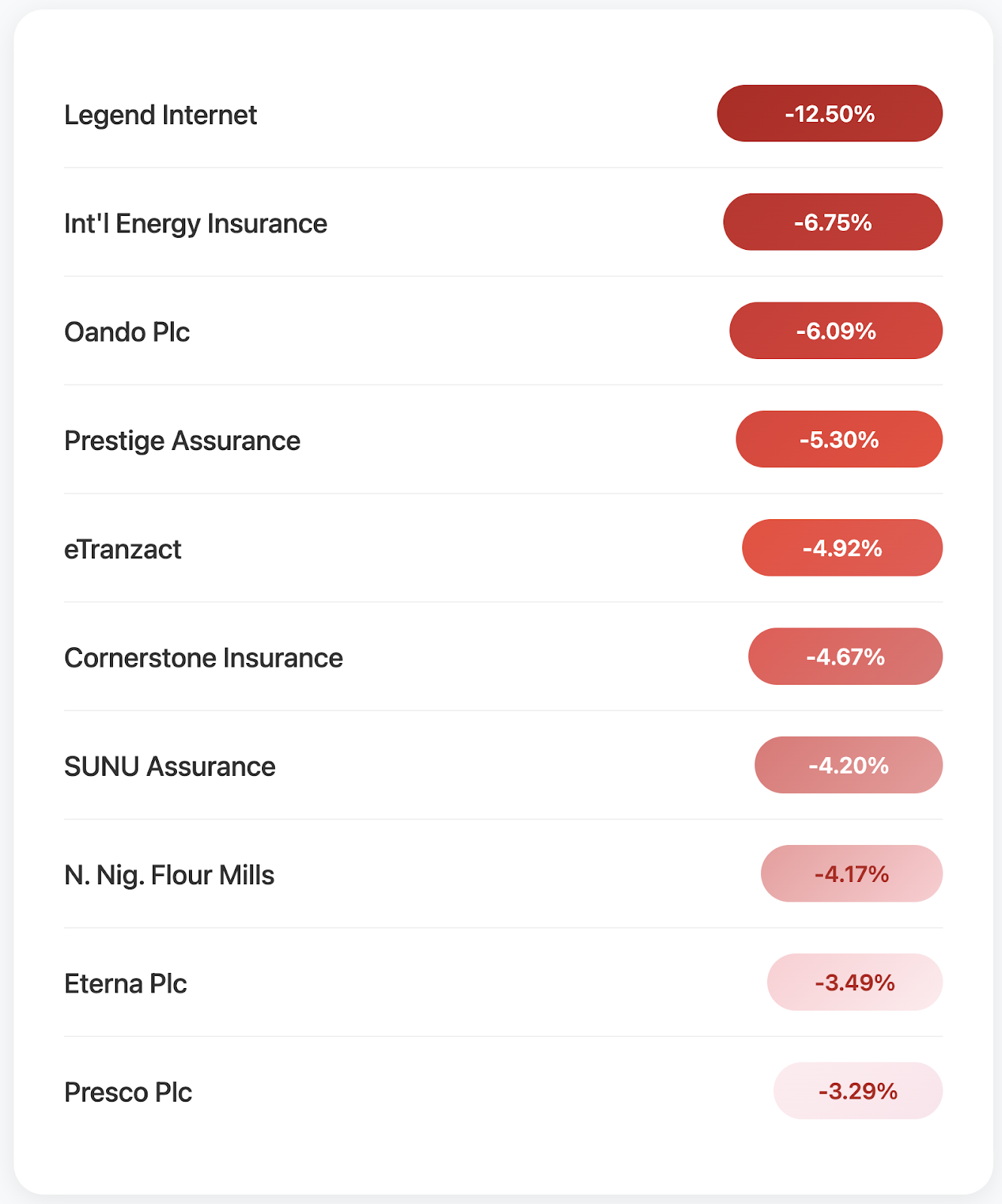

Top 10 Decliners

What it means: Losses were shallow, led by special-situation names (Legend Internet IPO drift) and oil stocks cooling after the Q2 spike. No systemic selling pressure detected.

Sector Performance Deep Dive

| Index | W-o-W % | Narrative |

| Banking | +13.83% | Rate-tailwind & GTCO share-issue enthusiasm drove tier-1 bid-up |

| Insurance | +8.14% | Dividend-capture and cheap valuations lured funds |

| Premium | +2.18% | Finally joined rally – breadth broadening a bullish omen |

| Consumer Goods | -0.72% | Defensive staples still grinding higher |

| -0.72% | -0.72 % | Consolidation after May/June out-performance |

Volume picture: Financials dominated 56% of shares and 52% of value, Oil & Gas slipped to 8%, and Services clocked in at 466 million shares (2.4% value). The cash-to-volume mismatch confirms large-ticket flows hunting liquidity in banks while small traders churned low-priced plays.

Volume & Value Analysis

- Top three by volume: Access Holdings, Japaul Gold, and AIICO Insurance, 1.396billion shares (25.9% of market volume) for ₦15.84 billion (14.7% of value).

- Cash kings: MTNN, Seplat, and Dangote Cement led naira turnover despite modest volumes, the perennial institutional magnets.

Investor psychology: Retail enthusiasm is alive in penny resources (Japaul), while institutions are doubling down on high-ROE banks and telcos.

Daily Market Progression

| Day | Deals | Volume (m) | Value (₦ bn) | Adv | Dec |

| Mon 7 Jul | 24,042 | 824.1 | 14.44 | 55 | 23 |

| Tue 8 Jul | 24,771 | 1,008.1 | 19.48 | 58 | 21 |

| Wed 9 Jul | 24,303 | 888.7 | 15.61 | 60 | 21 |

| Thu 10 Jul | 27,875 | 1,280.2 | 27.73 | 70 | 10 |

| Fri 11 Jul | 33,399 | 1,389.4 | 30.55 | 62 | 25 |

Inflection Day: Thursday’s breadth thrust (70/10) and ₦27 bn ticket signalled institutional FOMO, the catalyst that propelled the ASI beyond 125k.

Corporate Actions & Market Events

| Item | Detail |

| Ex-Div Adjustments | The June series (16.121 % 2027 & 17.121 % 2028) listed 9 Jul; liquidity light but yields attractive for treasury-ladder strategies. |

| FGN Savings Bonds | The June series (16.121% 2027 & 17.121 % 2028) listed on 9 Jul; liquidity is light, but yields are attractive for treasury-ladder strategies. |

| GTCO Share Listing | 2.288 billion new shares from public offer admitted 10 Jul – expands float, deepens banking liquidity pool. |

| ETPs | 242,901 units worth ₦22.43 m traded, up 19 % in value w/w – STANBICETF30 and GREENWETF led flows. |

| Bonds | 66,289 units (₦69.24 m) swapped – volume down 60 % as dealers stayed glued to equities. |

What does this means for your portfolio?

This week’s 4.26% NGX All-Share Index surge to 126,149.59, combined with 90 advancing stocks versus just 16 decliners, isn’t just another good week—it’s the market telling you exactly where institutional money is positioning for the earnings season ahead. Here’s how you should think about your holdings:

According to market dynamics observed in the NGX last week, the Financial Services sector’s dominance (56% of volume, 52% of value) signals serious institutional conviction. When you see 3.019 billion shares worth ₦56.244 billion flowing into banks and insurance in a single week, that’s not retail speculation—that’s smart money positioning for dividend announcements and Q2 earnings surprises.

The 17.121% yield on newly listed FGN Savings Bonds creates a fascinating dynamic: with risk-free returns this high, equity plays need to deliver exceptional value to justify the risk premium.

If You’re Conservative

The Insurance sector’s explosive 13.83% weekly gain to 904.12 wasn’t accidental. When defensive sectors lead while market breadth stays this strong, you’re watching institutions rotate into dividend sustainability ahead of half-year results.

Your Action Plan:

Lock in FGN Savings Bond yields: The June 2025 issue offers 17.121% over three years with quarterly payments. At these yields, allocate 40-50% of conservative assets here—this is the highest risk-free return available.

Insurance exposure on strength: AIICO Insurance dominated volume charts this week, contributing to the sector’s 13.83% surge. When insurance leads in a bull market, it’s usually dividend sustainability driving flows.

Banking profit-taking strategy: After the Banking Index’s 12.49% surge to 1,457.87, trail stop-losses at 5% below Friday’s close. Keep core positions in Access Holdings and GTCO for dividend capture, but protect gains.

Risk Management: With the All-Share Index at 126,149.59, just 1% from potential resistance, don’t chase momentum. Scale positions over 2-3 weeks if adding equity exposure.

If You’re Growth-Oriented

The NGX Premium Index’s 8.14% explosion while maintaining broad participation signals something fundamental is shifting. When you see companies like Nigerian Exchange Group deliver 54.85% in five days (₦46.40 to ₦71.85), that’s institutional money chasing growth at any reasonable price.

Your Opportunities:

Banking momentum trade: Access Holdings and GTCO led volume this week while the Banking Index surged 12.49%. With GTCO raising ₦160 billion through its public offer, fresh capital deployment could drive continued outperformance.

NGX Group breakout: The 54.85% surge from ₦46.40 to ₦71.85 represents a technical breakout after consolidation. Watch for a retest of ₦65 support before the next leg higher.

Mid-cap explosions: FTN Cocoa’s 60.60% gain (₦4.67 to ₦7.50) and Red Star Express’s 60.57% surge show institutions chasing overlooked industrial plays. This breadth across unrelated sectors means something bigger is brewing.

Your Risk: These moves are sharp and fast. The NGX Growth Index momentum requires strict position sizing—don’t bet more than 3-5% of your portfolio on any single momentum play.

If You’re Value Hunting

Sometimes the market overreacts, and patient investors get rewarded. This week’s few decliners offer compelling contrarian opportunities:

Your Shopping List:

Oando at ₦51.70: The 6.09% decline from ₦55.05 likely reflects downstream roadmap delays, but long-term oil infrastructure value remains intact. Entry around ₦50 offers asymmetric upside.

Presco post-dividend: Down 3.29% to ₦1,233 after paying ₦42 dividend—this is mostly ex-dividend adjustment creating artificial weakness. Medium-term value play for agricultural infrastructure.

Oil & Gas sector rotation: The NGX Oil/Gas Index’s 0.72% decline to 2,445.85 makes it the only major sector in the red. When defensive sectors outperform this strongly, energy often follows with catch-up moves.

The Contrarian Play: Legend Internet’s 12.50% drop represents technical selling rather than fundamental deterioration. Technology plays often recover quickly in momentum markets.

Sector Allocation Strategy

Based on this week’s flow patterns and the 17% bond yield backdrop, here’s how to position your portfolio:

Overweight (35-40%):

- FGN Savings Bonds: 17.121% risk-free beats most equity dividends

- Banking: 12.49% sector momentum with earnings catalysts ahead

- Insurance: 13.83% gain signals dividend sustainability focus

Neutral Weight (25-30%):

- Consumer Goods: 2.18% gain shows steady domestic demand

- Selected Growth Names: NGX Group and mid-cap momentum plays

Underweight (15-20%):

- Oil & Gas: Temporary weakness but watch for reversal above 2,500

- Industrial Goods: 2.94% gain lags market, value emerging

Your Week Ahead Action Plan

Immediate Moves:

- Scale into 17% FGN bonds if conservative income is priority

- Trail banking stops 5% below Friday close while maintaining core positions

- Build watchlists of oil & gas names for sector rotation entry

Key Levels to Monitor:

- All-Share Index: 126,149.59 needs to hold above 125,000 for trend continuation

- Banking Index: 1,457.87 must stay above 1,420 to maintain momentum

- Oil & Gas Index: Break above 2,500 signals sector rotation beginning

- Daily volume: Above ₦25 billion confirms institutional conviction continues

Forward-Looking Analysis

- Technical Roadmap: Immediate resistance sits at 127,000; a decisive close ≥127.5k sets a path to 130k by month-end. Initial support now 123,800 (Thursday’s gap).

- Catalysts:

- Bank earnings (14-18 Jul) – upside beat could extend sector melt-up; miss would spark swift rotation back to defensives.

- July CPI print (due 16 Jul) – any downside surprise ignites consumer-goods rally.

- Crude headline risk – Brent under $80 keeps pressure on Oil & Gas index.

- Bank earnings (14-18 Jul) – upside beat could extend sector melt-up; miss would spark swift rotation back to defensives.

- Breadth Watch: Sustain ≥60 advancers per day to keep rally intact; slip below 40/25 (adv/dec) would flag distribution.

- Liquidity Trigger: Keep an eye on daily value – staying north of ₦25 bn signals funds are still buying strength; sub-₦15 bn could mark exhaustion.

Bottom line for the week of 14 July: Momentum remains your friend, but new highs demand discipline. Let positions run, tighten stops, and be ready to rotate if bank results underwhelm.

The Bottom Line for Your Money

This week proved something fundamental: when the All-Share Index gains 4.26% while 90 stocks advance versus just 16 declining, you’re not seeing speculation—you’re watching institutional repositioning for earnings season and dividend announcements.

The math is compelling: Nigerian Exchange Group delivered 54.85% returns in five days by benefiting from increased trading activity. The Banking sector gained 12.49% on capital raising and earnings optimism. These aren’t lottery tickets—they’re quality businesses finally getting institutional recognition.

Your competitive advantage: While others chase yesterday’s winners, you can position where institutional money is flowing next. The 17% FGN bond yield provides an exceptional risk-free baseline, making equity risk premiums more attractive for quality names.

Whether you’re building wealth for retirement or trading for growth, this week reminded us why following institutional flow patterns—₦107.811 billion in weekly equity turnover—often beats trying to predict where headlines will take markets.

Please note that this analysis is based solely on NGX market data and does not constitute personalized investment advice. Always conduct thorough research and consider your risk tolerance before making any investment decisions.