Nigerian Stock Market Weekly Report

Week in review — Friday 18 July 2025

If you held BUA Cement shares last Monday morning at ₦94, you could have sold them Friday afternoon at ₦123.40, a cool ₦29.40 per share profit that would have paid for a nice dinner in Victoria Island. Multiply that by a few thousand shares, and you’re looking at the kind of week that changes portfolios.

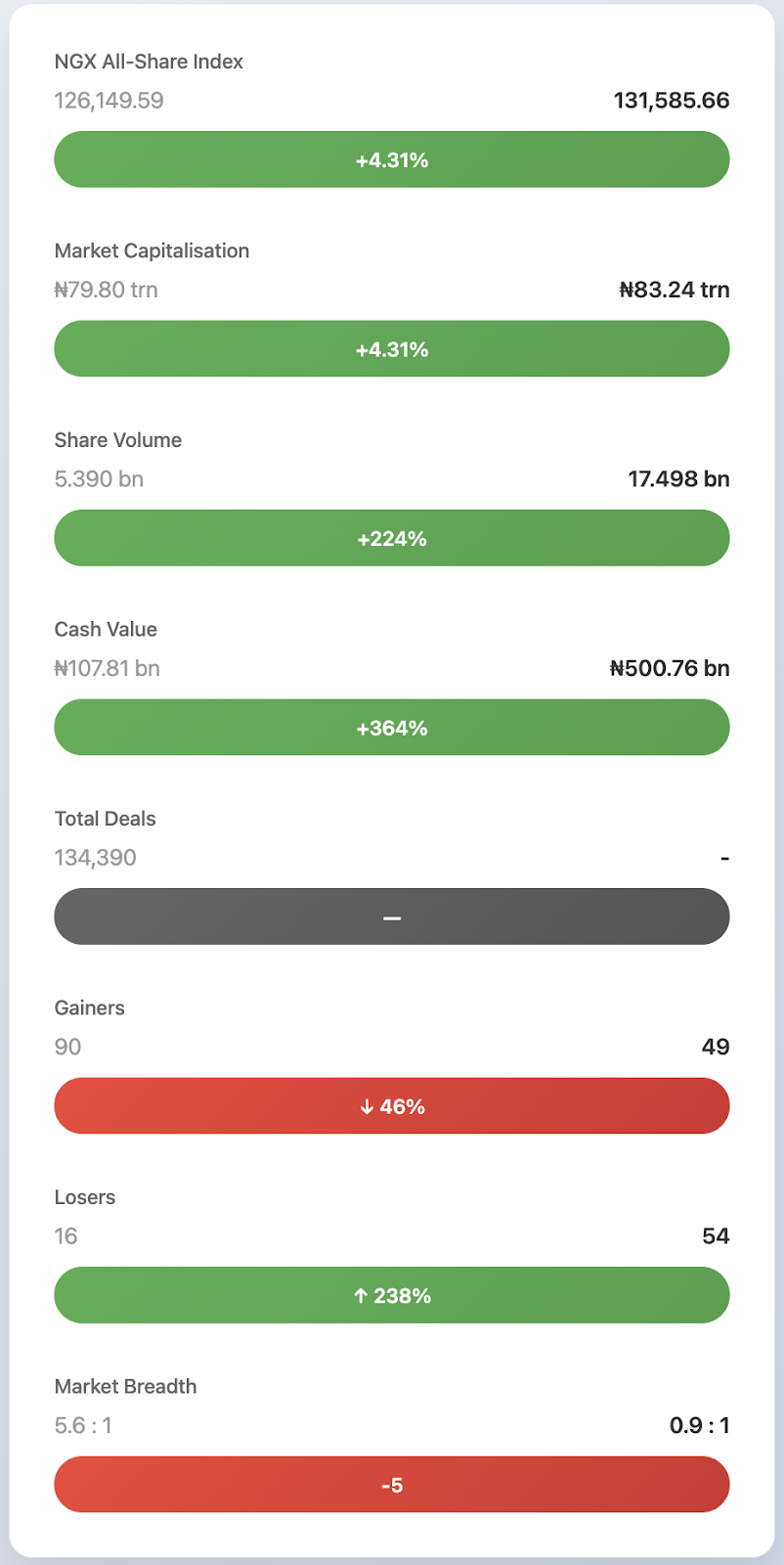

But here’s the thing that should keep every serious investor awake tonight: while you were celebrating that 31% BUA gain, institutional players moved 17.5 billion shares worth ₦500.8 billion in just four trading sessions. To put that in perspective, the volume is more than triple that of the previous week and nearly five times the value. In Lagos traffic terms, imagine Victoria Island handling five times its regular cars in 20% less time, something extraordinary was happening.

Tuesday was declared a public holiday for former President Buhari, leaving the market with only four days to work. Yet on Wednesday alone, just one day, ₦363.4 billion changed hands. That’s more money than many Nigerian states see in their entire annual budgets, flowing through the exchange in eight trading hours. When traders in Marina pushed that kind of volume while the All-Share Index climbed from 126,149 to 131,585 points, they weren’t gambling; they were positioning.

The numbers tell a story that many investors have overlooked. Yes, the headlines screamed about the index hitting new highs and ₦3.44 trillion being added to market capitalization. But dig deeper: 49 stocks gained while 54 declined. For the first time in five weeks, more stocks fell than rose, even as the market soared 4.31%. That’s not excitement, that’s surgical precision. Three banks, First Holdco, FCMB Group, and Fidelity Bank, accounted for 13.2 billion shares, or 76% of the total volume traded.

Think about it this way: if the entire Nigerian stock market were a restaurant, these three banks ordered three-quarters of everything on the menu while everyone else shared the remaining 25%.

When money moves that decisively, with that much concentration, someone with serious information is making serious bets. The only question is: are you following their playbook, or are you still reading yesterday’s menu?

You can read my stock market report for week 3 of July 2025 here.

Key Market Metrics Dashboard

Sources: NGX weekly summary

Market Analysis Narrative

Here’s what caught our attention: banks accounted for 90% of all shares exchanged and 87% of cash value. When one sector monopolises the tape, it usually means institutions are either positioning ahead of results or hedging macro risk.

The trio of First Holdco, FCMB Group and Fidelity Bank alone cleared 13.2 billion shares (76% of volume), confirming heavyweight accumulation.

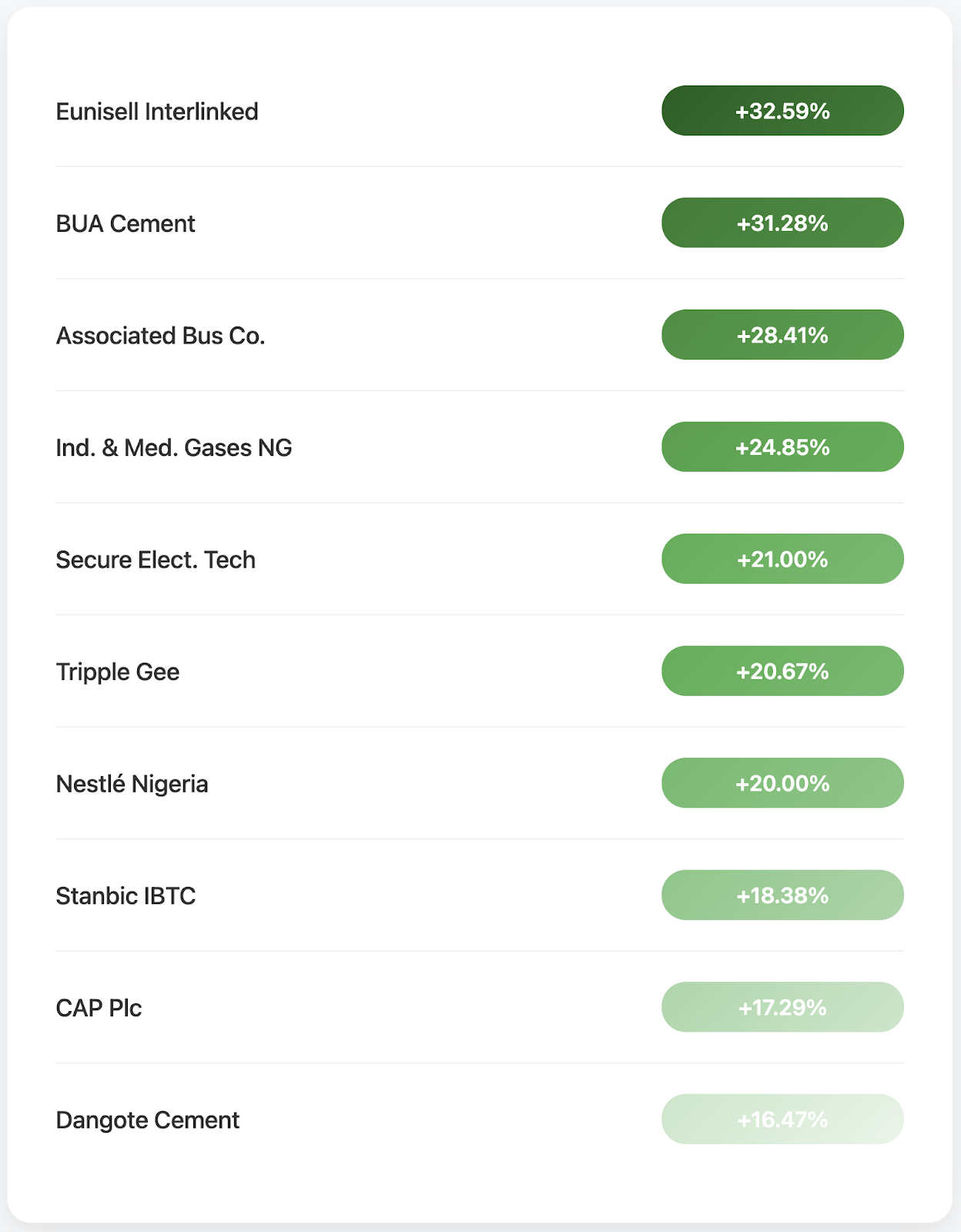

Yet price action was far from one-way bullish. Defensive mega-caps, such as BUA Cement (+31%) and Dangote Cement (+16%), lifted the Industrial Goods Index by a blistering 19.17%.

In contrast, the Insurance Index slipped 3.65%, while the Growth Index fell 4.8%, hinting that hot money rotated out of speculative plays into balance-sheet strength.

Daily tape-reading shows Wednesday’s session was the pivot: only 30 advancers vs 47 decliners, even as ₦42.8 billion crossed the tape. By Friday, bargain hunters returned (46 winners), but breadth remained fragile.

Why the divergence? Three catalysts dominated corridors in Marina:

- Liquidity glut — Rights-issue proceeds and maturing OMO bills found a temporary home in tier-one banks.

- Q2 earnings whisper — Early channel checks point to double-digit loan growth but thinning NIMs; traders front-ran any positive surprise.

- Rate-cut speculation — Softer June CPI (released mid-week) fuelled talk of a September MPR trim, juicing duration trades in cement and consumer blue-chips.

Put together, the pattern is clear: big money is getting quality exposure without abandoning equity risk, while quietly lightening up on high-beta names.

Winners & Losers

Top 10 Gainers

Data: NGX Top Price Gainers

Takeaway: Big-ticket cement and FMCG names led, signalling a flight to earnings stability. If you held BUA Cement you pocketed 31% in four sessions.

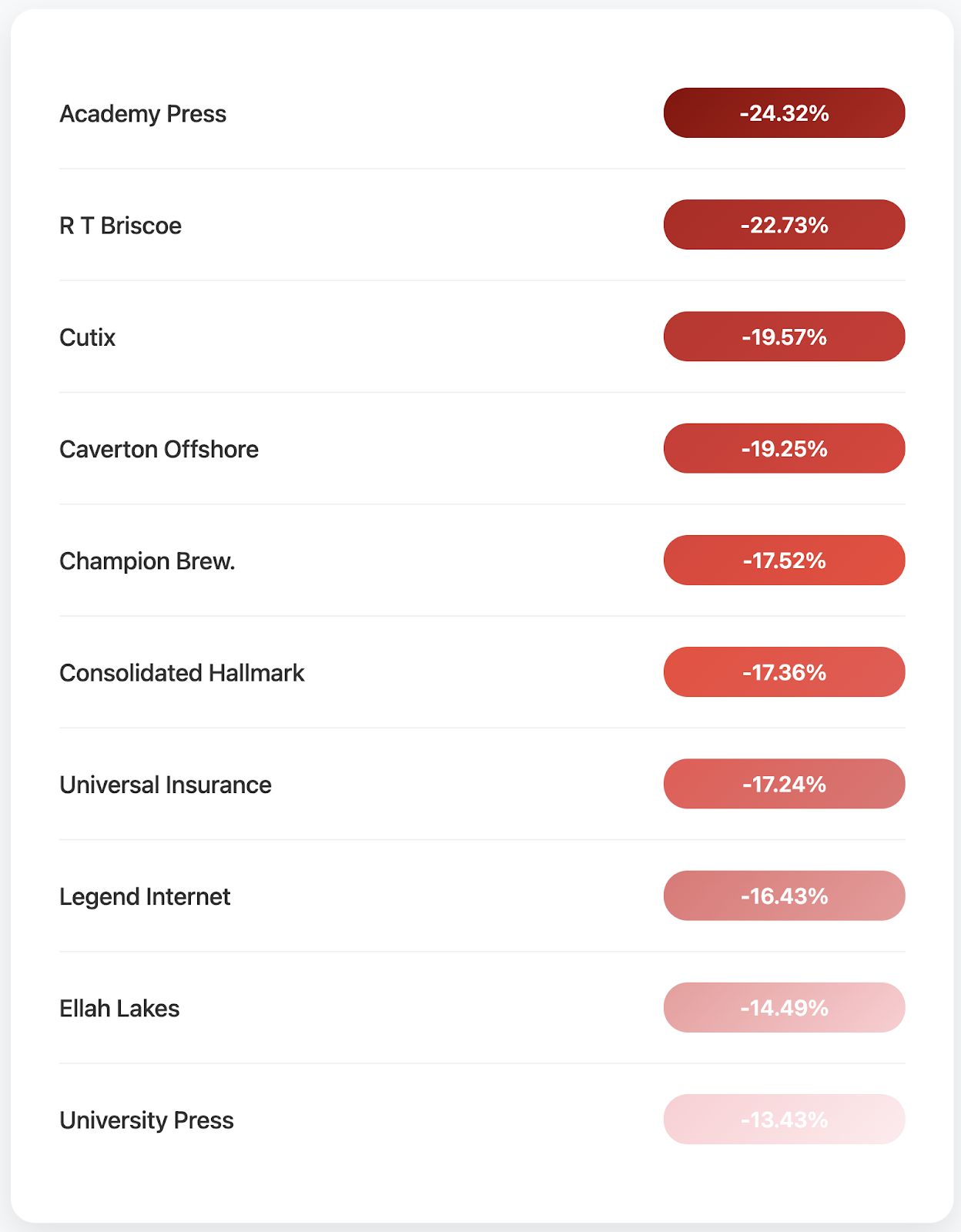

Top 10 Decliners

Data: NGX Top Price Decliners

What it means: Profit-taking battered micro-caps, especially publishers and transport plays, hinting at risk-off sentiment in speculative corners.

Sector Performance Deep-Dive

| Index | W/W % | YTD % | Note |

| Industrial Goods | +19.17% | 22.80% | Cement rally led by BUA & Dangote |

| Premium | +6.97% | 37.22% | Banks & telcos strongest clip |

| Banking | +5.36% | 41.64% | Liquidity magnet continues |

| Insurance | -3.65% | 21.33% | Claims inflation biting |

| Growth | -4.80% | 22.87% | High-beta rotation out |

Volume share confirms it: Financial Services, 90 %; ICT, 1.9%; Consumer Goods, 1.8%. Smart money is clustering in balance-sheet behemoths.

Volume & Value Analysis

- Three names (FBNH, FCMB, Fidelity) accounted for 75.6% of all shares and 73.4% of cash.

- Daily turnover peaked Wednesday at ₦363.4 billion, but breadth was the weakest (41 advancers vs 45 decliners) — a classic churn signal.

- ETF desk quiet: just 239,000 units were traded, worth ₦18.9 million (-16% w/w), indicating a risk appetite centred on equities, rather than hedges.

Daily Market Progression

| Date | Deals | Volume | Value (₦) | Adv / Dec |

| 14 Jul | 39,431 | 1.29 bn | 32.20 bn | 45 / 36 |

| 16 Jul | 36,639 | 11.67 bn | 363.41 bn | 41 / 45 |

| 17 Jul | 37,418 | 1.19 bn | 42.76 bn | 30 / 47 |

| 18 Jul | 28,594 | 3.35 bn | 62.39 bn | 46 / 25 |

Source: NGX daily turnover table

Wednesday’s liquidity surge with negative breadth marked the inflection; Friday’s bounce suggests dip-buyers are selective, not euphoric.

Corporate Actions & Market Events

Three price adjustments hit the tape:

| Company | Ex-Date | Dividend / Bonus | Adjusted Price |

| Linkage Assurance | 14 Jul 25 | 1-for-5 bonus | ₦1.33 |

| Fidson Healthcare | — | ₦1.00 cash | ₦46.00 |

| Jaiz Bank | 16 Jul 25 | ₦0.07 cash | ₦3.53 |

No new listings this week; the bond desk cooled with 34.5k units worth ₦31.5m (-55% value week-over-week).

What This Means for Your Investment Portfolio and Strategy

The Institutional Playbook: Follow the Volume, Not the Headlines

The week’s trading data reveals three distinct investment themes that should reshape your portfolio allocation:

Banking Sector Dominance (90% of volume): When institutions concentrate this heavily in one sector, they’re positioning for something big. The convergence of rights-issue proceeds, maturing OMO bills, and early Q2 earnings whispers suggests banks are becoming the preferred vehicle for institutional liquidity deployment. For individual investors, this signals an opportunity to average into tier-one banks on any 2-3% pullbacks, targeting dividend yields that remain north of 10%.

Infrastructure & Materials Play: The explosive gains in BUA Cement (+31%) and Dangote Cement (+16%) weren’t random speculation; they represent institutional positioning ahead of potential interest rate cuts. With June CPI data suggesting monetary policy may shift in September, cement and heavy industry stocks are being accumulated as duration plays. The 19.17% surge in the Industrial Goods Index confirms this thesis.

Quality Flight from Growth: The simultaneous 4.8% decline in the Growth Index, while blue-chips rallied, tells a clear story: Institutions are rotating from high-beta, speculative plays into balance sheet strength. This creates a two-pronged opportunity: quality at reasonable prices in the blue-chip space, and eventual mean-reversion opportunities in oversold growth names.

Tactical Positioning for the Next 30 Days

Conservative Allocation (40-50% of portfolio):

- Banking Overweight: Target FBNH, Stanbic IBTC, and Access Corp on any weakness below current levels. The sector’s 41.64% YTD performance combined with dividend yields above 10% offers both growth and income.

- Defensive Infrastructure: Build positions in Dangote Cement and BUA Cement using a dollar-cost averaging approach, targeting any pullback to 8% below recent highs.

Growth Allocation (25-30% of portfolio):

- Contrarian Insurance Play: With the Insurance Index down 3.65% while trading 18-20% off recent highs, consider nibbling on NEM Insurance and other low P/B leaders after Q2 results are published.

- Selective FMCG Exposure: Nestlé Nigeria’s 20% weekly gain suggests a renewed appetite for consumer defensive stocks. Monitor for entry points in Nigerian Breweries and Unilever Nigeria.

Opportunistic Allocation (20-25% of portfolio):

- Oil & Gas Mean Reversion: The sector’s modest 0.76% decline while crude oil holds above $80 presents a contrarian opportunity in names like Seplat Energy and Total Nigeria.

- Technology Recovery: ICT stocks represented only 1.9% of volume, suggesting institutional neglect that could reverse quickly with any positive sector catalyst.

Risk Management and Exit Triggers

Bull Case Continuation Signals:

- NGX-ASI holding above 129,000 support

- Banking volume maintains above 5 billion shares per session

- Market breadth returning to 60+ advancers on volume exceeding 3 billion shares

Bear Case Warning Signs:

- Break below 129,000 ASI support on volume above 10 billion shares

- Banking sector volume dropping below 70% of daily turnover

- Breadth deteriorating to fewer than 40 advancers for three consecutive sessions

Position Sizing Framework:

- Maximum single stock exposure: 8% of portfolio

- Sector concentration limit: 35% (except banking at 40%)

- Cash reserve: Maintain 15-20% for opportunistic deployment

The message from this week’s institutional activity is clear: Nigeria’s financial elite are positioning for a fundamentally different market environment.

The question isn’t whether to participate, but whether you’ll follow their playbook or get caught chasing yesterday’s winners. The volume patterns, sector rotation, and breadth dynamics all indicate a market in transition – one where patience and institutional alignment will distinguish the winners from the crowd.

Forward-Looking Analysis

Watch these triggers heading into the week of 21 July:

- Q2 bank earnings — A beat could push NGX Banking above 1,600.

- Policy chatter — Any hint of an August rate cut may extend the cement rally.

- Breadth reversal — A return to >60 advancers on volume >3 bn shares would confirm risk-on.

- Oil & Gas bounce — Sector down 0.8%; crude above $80 could spark mean reversion.

Key technical levels: ASI support 129,000; resistance 133,000. Keep eyes on liquidity — follow the money, not just the headlines.

Please note that this analysis reflects market observations and institutional patterns, rather than personalized investment advice. Always conduct your due diligence and consider your risk tolerance before making investment decisions.