When a Lagos commuter taps a Verve card at a POS machine to buy breakfast, or when a trader in Onitsha accepts a bank transfer from a customer, what appears to be a simple exchange is, in fact, a choreography of invisible infrastructure.

At the heart of this choreography lies the “switch” – a silent traffic officer that ensures money moves from one financial institution to another, instantly and securely.

In Nigeria, switches are the unsung heroes of digital payments. They carry the weight of every ATM withdrawal, every debit card swipe, every interbank transfer. “Think of them as the nerve system of Nigeria’s payment ecosystem,” says David, a senior executive at one of Nigeria’s top fintechs. “Without switches, the system collapses.”

A handful of players dominate the Nigerian landscape. Interswitch, founded in 2002, is often referred to as the pioneer, having given the country its first truly interoperable ATM network and later giving birth to Verve – Africa’s only homegrown card scheme.

Alongside it sits UPSL (Unified Payments Services Limited), Etranzact, and the ever-present NIBSS, whose Instant Payments (NIP) rails process trillions of naira every year.

Switches are the traffic controllers of digital money. They decide where each transaction should go, check if the customer really has funds, and ensure the right bank or wallet gets credited. Without them, interoperability collapses: Bank A can’t “talk” to Bank B, a card transaction fails, or a fintech app hangs at checkout.

For operators, especially financial services founders and payments teams, switches are not optional infrastructure. They are the backbone of scale, trust, and reliability in Nigeria’s fast-evolving financial ecosystem.

This playbook unpacks the what, who, and how of payment switches in Nigeria, offering step-by-step guidance for integration, partner selection, and operational excellence.

What is a switch?

At its core, a switch is a transaction-routing engine. Imagine it as the digital equivalent of a road interchange: cars (transactions) come in from multiple roads (banks, apps, POS devices), and the switch directs them to their correct destination quickly and safely.

Core functions:

- Transaction routing – Determines where the transaction should be directed (Bank A, Bank B, card scheme, or wallet).

- Authorisation – Validates customer credentials (PIN, OTP, CVV, biometrics) and checks account balances.

- Settlement & reconciliation – Moves money between institutions and provides reporting for operators.

- Value-added services – Fraud detection, tokenisation, bill payments, airtime recharge, loyalty schemes.

But beyond the technical layer, switching in Nigeria is a regulated business. Owning and operating a switch requires meeting the Central Bank of Nigeria’s (CBN) Switching and Processing licence requirements, one of the highest tiers in the payment ecosystem.

Basic Business Requirements for a Switching Licence (CBN, 2021)

To qualify for a Switching & Processing Licence, an applicant must meet both capital and operational thresholds, including:

- Minimum Paid-Up Share Capital: ₦2 billion ($1.37 million)

- Non-Refundable Application Fee: ₦100,000 ($68.6).

- Licence Fee (Payable Upon Approval): ₦1 million ($686).

- Evidence of Business Incorporation with CAC and certified Memorandum & Articles of Association.

- Detailed Business Plan including three-year financial projections, system architecture, risk management, and data security frameworks.

- Evidence of Payment System Infrastructure Readiness, including disaster recovery sites and PCI-DSS certification.

- Fit-and-Proper Directors and Shareholders, as assessed by the CBN.

These requirements ensure that only well-capitalised, technically competent, and compliant entities operate switches in Nigeria.

Switch vs Processor

- A switch connects different financial institutions, ensuring interoperability.

- A processor handles transaction execution for a specific institution or card issuer.

- In Nigeria, some entities (e.g., Interswitch) act as both.

What a switch enables: A technical view

To decide what switch(s) you need, you must understand exactly what functionalities, performance characteristics, and features you’re relying on. Below is a more detailed mapping of what switches provide (or should provide) in a robust system.

| Capability | Description | Key Performance / Technical Requirements |

| Transaction Routing / Switching | Determines whether a payment should go via bank-to-bank rail (like NIP), card network, POS network, etc. | Low routing latency (<50ms ideally), high throughput (thousands per second), ability to adapt dynamically (fallbacks). |

| Authorisation / Verification | Checks instrument (card/wallet), credentials (PIN, OTP, biometric), and fraud scoring | Secure APIs, PCI compliance if card data is handled, fraud systems, and possibly tokenisation. |

| Settlement & Reconciliation | Moving funds, net settlement across entities, reconciling mismatches, managing chargebacks/disputes | Clear settlement cycles, transparent reports, padding for exceptions, automated reconciliation, and audit trails. |

| Value-Added-Rails / Support | USSD, QR-code, mobile wallet interoperability, cross-border, proxy IDs (e.g. via BVN or similar), tokenisation | Multi-channel support, EMV & QR standards, ISO messaging (future-proofing), good APIs, monitoring tools. |

| Operational Resilience / Redundancy | Failover in case of switch failure, multi-switch backup, disaster recovery, and consistent uptime | Redundant infrastructure, geo-diversity, failover switching, high SLA (99.9–99.99%), and early warning/monitoring. |

| Compliance & Security | KYC, AML, PCI-DSS, data security, auditability, regulatory reporting | Secure encryption, audit logs, compliance with CBN and global standards, data protection, certification renewals. |

Mapping Nigeria’s switching landscape

Nigeria’s switching industry has matured over two decades. Four players dominate, each with a distinct role: Although, Four players seem to dominate the landscape processing over 80% of all switched card and POS transactions nationwide, Nigeria’s switching space has a strong mix of established and emerging players enabling and facilitating payments:

- Interswitch

- Founded in 2002, a pioneer of e-payments in Nigeria.

- Runs the Verve card scheme (the largest domestic card brand).

- Provides robust POS and ATM integrations.

- Expanding regionally into East Africa.

- UPSL (Unified Payments Services Ltd)

- Licensed by CBN as a national switch.

- Processes Visa, Mastercard, and Verve.

- Runs PayAttitude, an NFC/contactless scheme.

- Favoured by fintechs seeking multi-scheme flexibility.

- Etranzact

- Publicly listed on NSE.

- Strong with mobile money, agency banking, and telco partnerships.

- Powers “pocket banking” solutions across retail networks.

- NIBSS (Nigeria Inter-Bank Settlement System)

- Owned by CBN and all licensed banks.

- Runs NIP (Instant Payments), BVN, and TIPS.

- Less commercial, but unavoidable for interbank transfers and KYC.

- ChamsSwitch Ltd

- One of Nigeria’s earliest indigenous switching companies.

- Provides e-payment routing, card personalisation, and identity-management solutions.

- Licensed by the CBN as a national switch with focus on government and corporate payments.

- Strong in e-ID and public-sector transaction processing.

- 3Line Card Management Ltd

- A CBN-licensed switch and processor offering the Freedom Network for agency banking.

- Provides card management, POS switching, and wallet solutions for MFIs and fintechs.

- Known for deep rural-network coverage and SME-focused integrations.

- Xpress Payments Solutions Ltd

- Provides switching, processing, and payment-gateway services.

- Well regarded for high uptime and responsive API support.

- Expanding partnerships with banks and fintechs for real-time settlement and card services.

- Focuses on digital-first institutions seeking flexible integration models.

Other recent entrants include the likes of Paystack, Flutterwave, and Zone have also entered the switching game.

Operator Insight: Fintechs rarely have the luxury of “picking one.” Most end up integrating with at least two for redundancy.

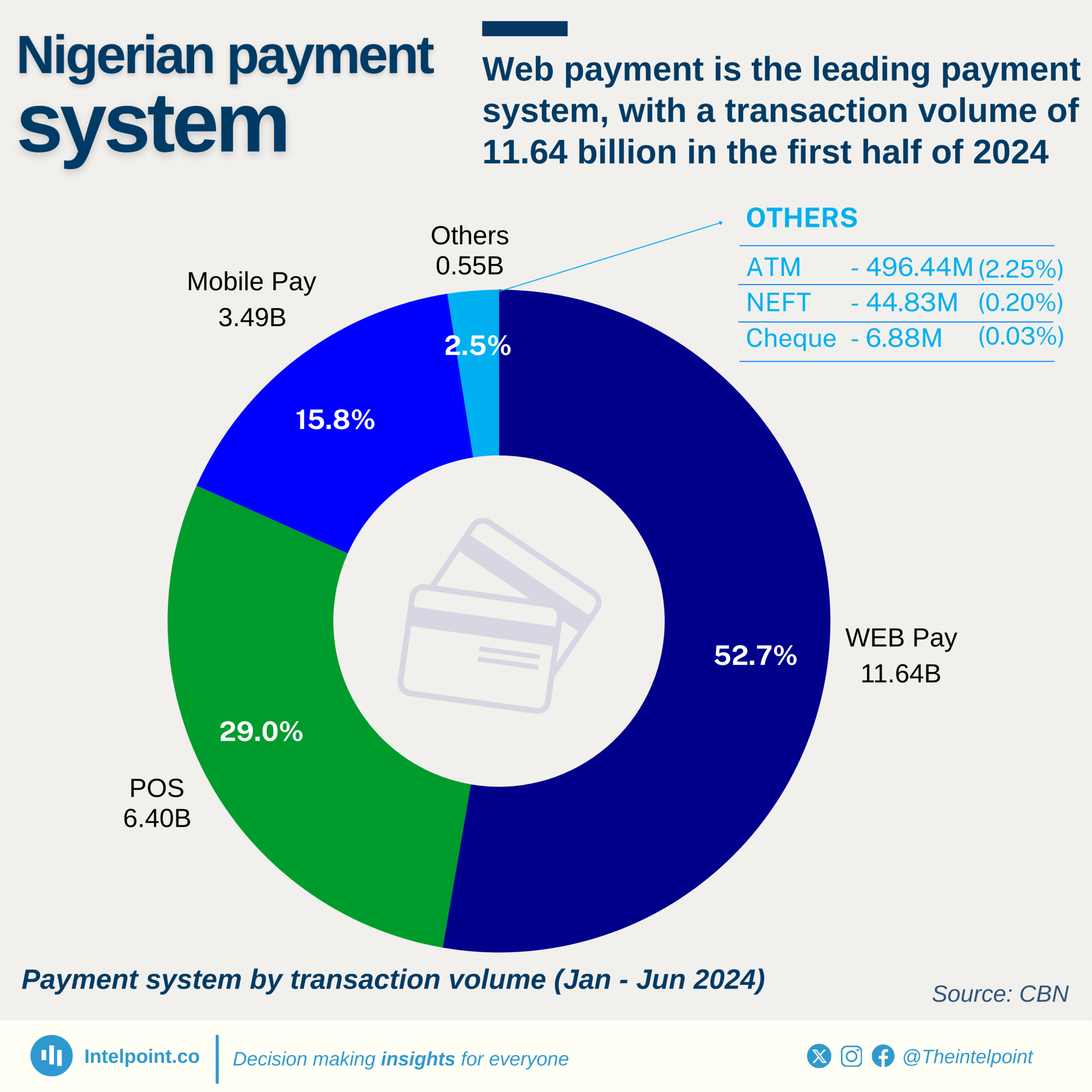

In 2024, Verve cards accounted for ~40% of active cards in Nigeria, while Visa/Mastercard made up the rest. That split influences whether operators lean more heavily on Interswitch or UPSL.

Scenario-based switch strategies

Different product types/business models will benefit from different switch configurations. Below are scenarios, trade-offs, and recommended strategies.

| Scenario | Key Requirements | Recommended Switch Strategy | Trade-Offs |

| Neobank issuing domestic debit cards + international cards | Card scheme support (Visa/Mastercard), POS & ATM access, card issuing, card-domestic + cross-border routing, lots of web payments | Use: Dual-switch model — e.g. Interswitch for Verve domestic + local POS/ATM, UPSL (or partner) for Visa/Mastercard issuance / international acceptance. Also, ensure good fallback routing. | Complexity of integration rises; cost of issuing multiple cards; reconciliation across switches; possible overlapping fees. |

| Bill payments / Utilities / Merchant-facing service | High POS/web traffic; stable, low-cost per transaction; reliability; low latency; minimal card issuance | Use: A switch with wide POS support + web API focus; possibly partner with UPSL if multi-scheme needed; ensure fallback via NIP or bank transfer for large payments. | Merchant service providers often face disputes, refunds, POS failures are painful, and margins may be thin. |

| Mobile money / Wallet + Agent Banking | Offline / low bandwidth support; integration with telco/MMO; POS, USSD, QR; perhaps less reliance on card rails, but with an option; settlement risk; liquidity management | Use switch(s) strong in mobile / wallet integration (Etranzact, hybrid); ensure NIP access; possibly use web rails for large value settlements; build API resilience. | More moving parts; risk of provider lock-in; need careful handling of float / regulatory requirements; possibly lower per-transaction fees but more operational overhead. |

| Cross-border expansion (West/East Africa) | Multi-currency, cross-border settlement, regulatory compliance in multiple jurisdictions, cards, possibly SWIFT or correspondent banking, and real-time rails | Partner with switches with existing regional presence (e.g. Interswitch if expanding), or use local switches + correspondent; design your product so domestic switch logic is modular; possibly use ISO 20022 readiness. | Significant regulatory complexity; currency risk; increased cost. |

Integration deep dive

A technical roadmap of what you should expect/build, and what you should demand of a switch partner.

A. Transaction routing & fallbacks

- Route by transaction type: (card vs account transfer vs wallet).

- Build fallback paths:

- If the primary switch fails for POS, redirect to the secondary switch (if available).

- If the card scheme is down, fall back to bank transfer/wallet.

- Real-time monitoring & health checks for each switch endpoint.

B. Settlement cycles & net vs gross settlement

- Understand the settlement frequency of each switch/rail (NIP now settles 4x/day; card schemes may settle daily).

- Know whether the settlement is gross or net: net means risks of settlement mismatch/float arise.

- Be clear on deferred net settlement risk, especially for large values or international cards.

C. API & technical standards

- APIs should support: synchronous & asynchronous modes, webhooks, retry semantics, and idempotency.

- Standard message formats: ISO 8583 (card rails), ISO 20022, where applicable; fields for metadata/fraud detection.

- Security: TLS, encryption at rest, tokenisation, especially for card data (if handling PANs).

D. Latency, throughput & performance

- Aim for under 100ms for internal routing (once authentication reaches the switch), and under 1-2 seconds for a full user-facing response (card POS/web). For NIP, many succeed in ~10 seconds.

- Throughput testing: Simulate peak loads and ensure the switch partner provides load testing data.

- Monitoring tools: error rate dashboards, latency percentiles (p95, p99), fallback usage.

E. Reconciliation & dispute management

- Reconciliation: daily/real-time matching of expected vs processed transactions, failed vs successful, merchant settlement.

- Dispute/chargeback workflows: especially for card transactions; clarity on who owns which stage of dispute, timing, and cost.

- Reporting & audit trails: logs with unique IDs, timestamps, and versioning.

F. Redundancy / Resilience

- Secondary switch partner (or more) for key rails.

- Geo-redundant data centres/disaster recovery plans.

- Health-check monitoring, alerting for failures, and automatic failover (if feasible).

Operator Checklist (with Technical & Contractual Questions)

| Area | Questions to Ask / Items to Verify |

| Licensing & Scheme Access | Is the switch licensed for switching & processing by CBN? What card schemes does it support? Do they support international cards if needed? |

| Latency & Throughput Guarantees | What is the SLA on latency for different channels? What is the throughput (TPS) tested? How do they handle peak traffic? |

| Settlement Terms | How often is a settlement done? Net vs gross? What are the cutoff times? What are the cycle windows? |

| Fee Structure | What are per-transaction fees by channel (POS, web, card, transfer)? Are there fixed fees, variable fees, or monthly minimums? Hidden costs? |

| API/Integration Support | Access to sandbox environments, documentation, versioning, webhooks, retry semantics, and idempotency. |

| Resilience/Backup | Do they have secondary switch options? Geo redundancy? DR (disaster recovery) paths? Failover strategies? |

| Compliance/Security | Is the switch PCI-DSS certified? Do they handle card data (PAN) or tokenise? How is data encrypted, stored? What are their breach protocols? |

| Reconciliation & Dispute Management | Is there a merchant/fintech dashboard for reconciliation? What is the timeline for handling failed transactions, chargebacks, and refunds? |

| Monitoring & Transparency | Do they provide dashboards for latency/error rates/uptime? What historical downtimes or incidents have occurred? |

| Regulatory & Consumer Protection | Fee disclosure, dispute resolution processes, customer recourse, compliance with CBN’s guidelines (on charges, consumer rights). |

Integration Flow Diagram: Switch Onboarding & Go-Live

| [Fintech / Operator] | (1) Define transaction needs | v [Shortlist Switch Partners] | (2) Evaluate SLAs, Fees, API Docs, Compliance | v [Sponsoring Bank Partner] —– | | | (For NIBSS / NIP access) v | [Switch Provider API] <—— | (3) Sandbox Testing – Authentication – Routing logic – Error handling – Reconciliation flows | v [Certification & Approval] – CBN compliance – Scheme (Visa/Mastercard/Verve) – PCI-DSS / ISO standards | v [Pilot / Limited Rollout] – Test with real users – Monitor latency/failures – Daily reconciliation | v [Production Go-Live] – High volume routing – Fallback paths active – Real-time monitoring | v [Settlement & Reconciliation] – Net/gross settlement windows – Bank settlement accounts – Automated dashboards | v [Ongoing Operations & Support] – Dispute handling – SLA monitoring – Regulatory reporting |

Switches are the invisible scaffolding of Nigeria’s payments industry, rarely seen by end-users, but indispensable to every fintech founder, bank, and merchant. They decide whether transactions succeed or fail, and by extension, whether customers trust your product enough to keep using it.

For operators, the path is clear: treat switch integration not as a box-ticking exercise, but as a core strategic decision. The right partner(s), backed by redundancy, clear SLAs, and robust reconciliation, will set the foundation for scale. The wrong choice, or a lack of backup, can cripple growth overnight.

As Nigeria’s payments ecosystem races ahead, with trillions flowing through NIP, millions of POS terminals in circulation, and ISO 20022 reshaping transaction data, the winners will be those who build resilient, compliant, and customer-centred integrations.

Switches may be silent, but their impact is loud: in uptime, in customer trust, and in the difference between fintechs that stumble and fintechs that scale.