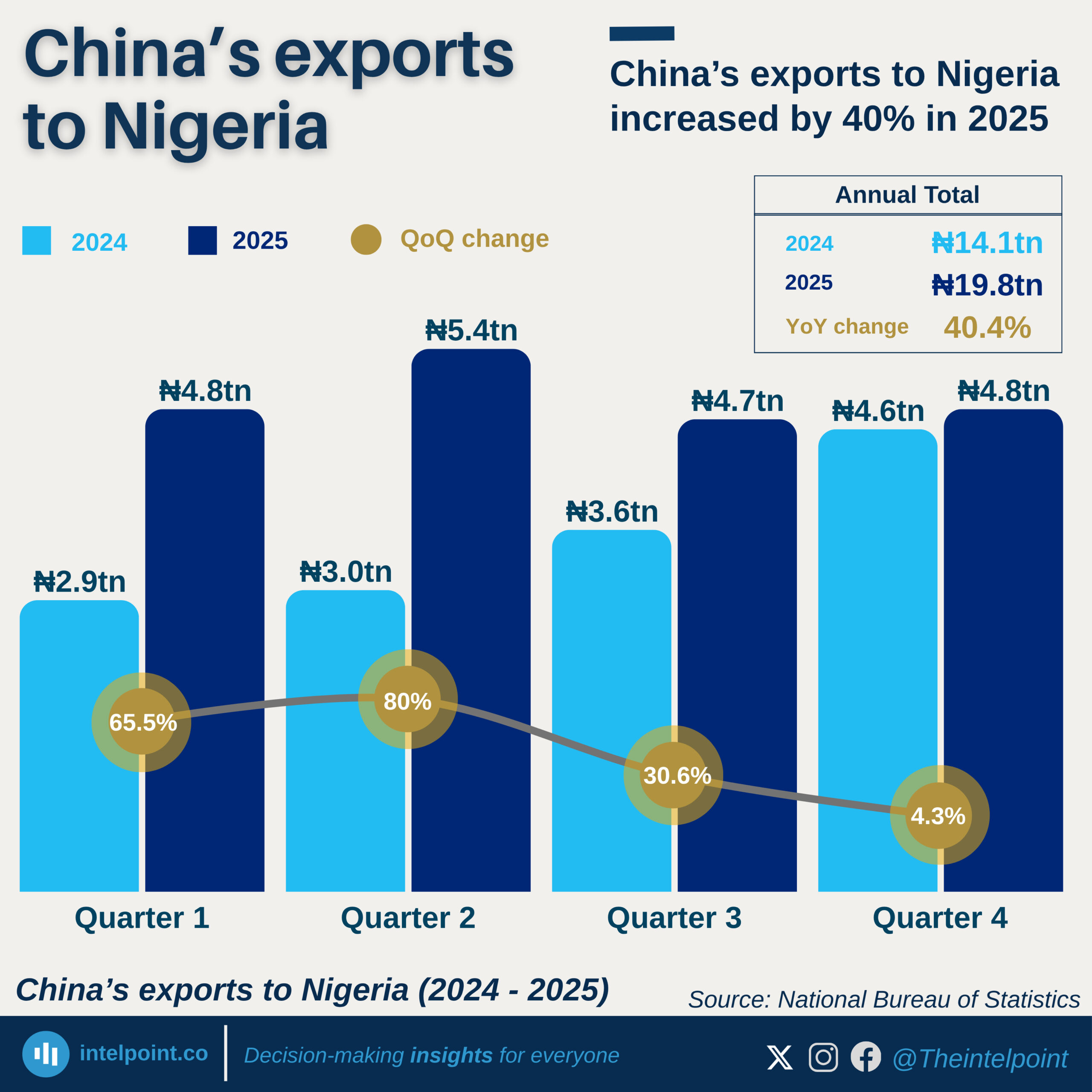

Nigeria’s imports from China rose sharply in 2025, underscoring the Asian country’s growing dominance in the West African nation’s trade economy and the persistent imbalance in bilateral flows.

Data from the National Bureau of Statistics (NBS) analysed by Finance in Africa shows that imports from China increased by 36.7% to $13 billion (₦19.8 trillion), up from $9.5 billion (₦14.1 trillion) in 2024. The figure represents more than a quarter of Nigeria’s total import bill of $46.7 billion (₦64.1 trillion) during the period.

The increase reflects sustained demand for industrial goods and machinery, alongside Nigeria’s continued reliance on external manufacturing to meet domestic and infrastructure needs.

Import growth driven by industrial demand

Quarterly data shows a strong build-up in import values through the year, rising from $3.14 billion (₦4.7 trillion) in the first quarter to $3.61 billion (₦5.4 trillion) in the final quarter. The trend indicates consistent demand despite exchange rate pressures and tighter financial conditions.

China remained the primary source of industrial inputs. Key imports included machinery for data transmission valued at $439 million (₦657.1 billion), solar cells worth about $244 million (₦365.6 billion) and plant equipment and herbicides of $244 million (₦365.6 billion), as well as other capital goods used across manufacturing and infrastructure.

The composition of trade highlights the extent to which Nigeria depends on imported inputs to support production and economic activity, particularly in sectors where domestic capacity remains limited.

Trade imbalance remains entrenched

While imports from China have expanded, Nigeria’s exports to the country remain comparatively low, continuing a long-standing pattern of trade imbalance.

Although recent export figures to China were not disclosed, historical data shows a consistent surplus in Beijing’s favour. Nigeria recorded an $18 billion trade deficit with China in 2023, reflecting the wide gap between inbound manufactured goods and outbound primary commodities.

The structure of trade has remained largely unchanged, with Nigeria exporting mostly raw materials while importing higher-value finished and semi-finished goods.

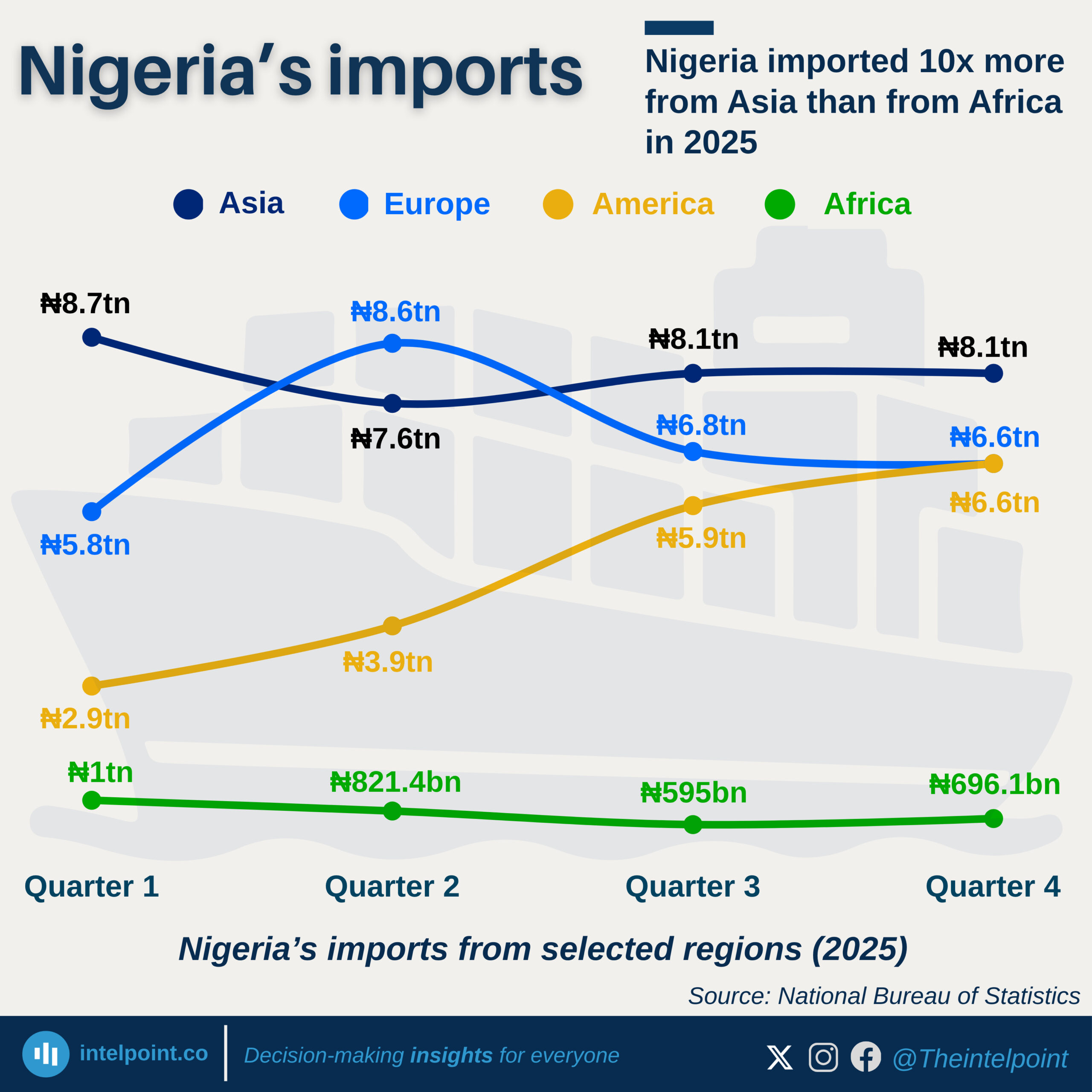

Asia leads as trade patterns diverge

China’s position reflects a broader regional trend where Nigeria records trade deficits with manufacturing hubs and surpluses with commodity-linked partners.

Consequently, Asia remained the West African nation’s largest source of imports in 2025, accounting for $21.7 billion (₦32.5 trillion), up from $18.2 billion (₦20.9 trillion) in 2024.

By contrast, Europe—Nigeria’s second-largest import partner—saw a more modest increase of 6%, with exports to the African economy reaching $14.4 billion (₦21.6 trillion). Nigeria maintained a trade surplus with the region estimated at $5.9 billion, supported by stronger export flows.

Trade with the Americas expanded significantly, more than doubling to $16.9 billion (₦25.3 trillion), with imports and exports relatively balanced at $8.3 billion (₦12.4 trillion) and $8.6 billion (₦12.9 trillion) respectively.

Within Africa, Nigeria continued to record a strong surplus, with exports rising to $8.7 billion (₦13 trillion) from $6.2 billion (₦9.3 trillion) in 2024, led by key partners including South Africa and Togo.

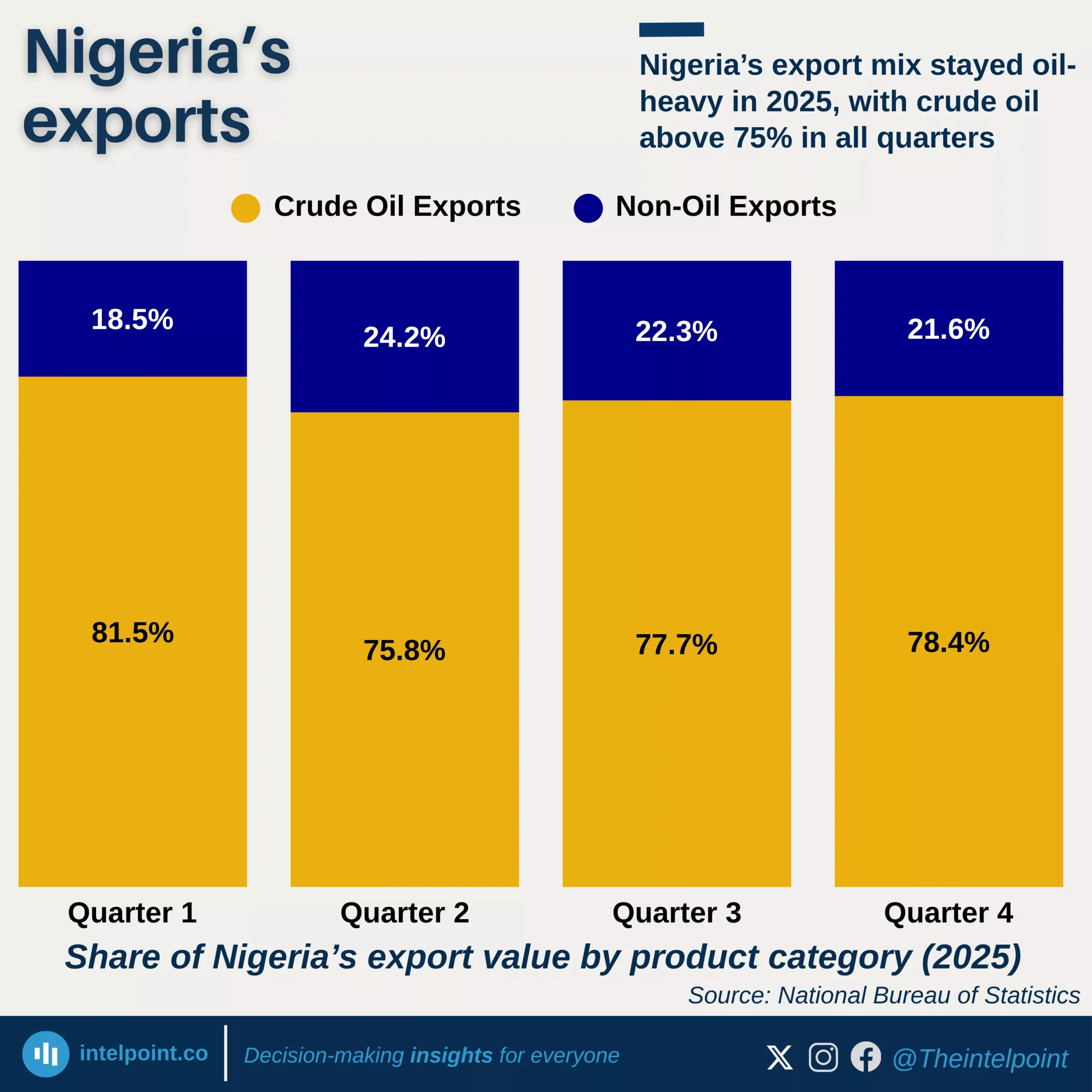

Oil sustains surplus even as rising imports deepen FX pressures

Nigeria recorded a trade surplus of $13.7 billion (₦21 trillion) in 2025, as higher crude oil shipments lifted total exports by 9.8% year-on-year to $55.9 billion (₦85 trillion).

Still, import spending increased, mounting pressure on the country’s foreign reserves and local currency. Despite showing early signs of stability during the year, the naira remained one of the weakest African currencies, stronger than only seven of 41 as of October.

Anchoring this fragile recovery were oil exports, which stood at $30.9 billion (₦46.3 trillion) — accounting for 55% of total export earnings and reinforcing the commodity’s role as the country’s main source of foreign exchange.

This performance came despite a decline in global oil prices over the year, with Brent crude falling from $79 per barrel in January to $63 in December. At the same time, non-oil exports contributed just 20% of total shipments, indicating limited progress in diversifying Nigeria’s export base despite ongoing policy efforts.

Why China remains Nigeria’s top supplier

China’s position as Nigeria’s leading source of imports reflects a combination of pricing, scale and supply chain advantages.

Chinese goods are generally more affordable, making them attractive in a cost-sensitive market. In addition, Beijing’s extensive manufacturing base ensures steady supply across a wide range of sectors, from consumer goods to heavy machinery.

Bilateral engagement has also strengthened over time, supported by infrastructure financing and trade initiatives under China’s Belt and Road framework. A recent policy offering duty-free access to 53 African countries, including Nigeria, is expected to further deepen trade ties amid strained U.S-Africa relations.

However, analysts warn that the impact of the policy may be limited in the near term, as most African exports to China are primary commodities that already face minimal tariffs.

“For most of the continent, the practical change is smaller than the headline suggests,” US-based DW news said in a recent report.

“The goods that would genuinely benefit — processed food, manufactured items, textiles — are precisely those which African economies struggle to produce at scale.”

Risks linked to concentration

The concentration of imports from a single market presents potential risks.

Nigeria’s reliance on Chinese goods exposes it to external shocks, including changes in China’s economic conditions, supply chain disruptions or shifts in trade policy.

There are also implications for the domestic industry. Continued dependence on imported inputs may slow the development of local manufacturing, particularly in sectors where Nigeria has the potential to build capacity over time.

Concerns have also been raised in some quarters about quality standards in imported goods, particularly in infrastructure-related projects, though these vary across sectors.

Structural constraints limit adjustment

Addressing this imbalance will require sustained investment in infrastructure, including power, transport and logistics, to reduce production costs and improve competitiveness.

Strengthening human capital and technical capacity will also be important in supporting industrial development.

While diversifying trade partnerships could reduce concentration risks, such adjustments are gradual and depend on improvements in domestic production capabilities.

Until Nigeria builds domestic industrial capacity, trade with China will remain less a partnership and more a structural dependency – one that continues to shape the country’s FX stability and growth trajectory.